A new regime arrives for UK private fund managers

Published on 30th June 2025

What are its main features, what does it mean for fund managers and what's to be addressed to ensure its future success?

HM Treasury and the Financial Conduct Authority (FCA) have unveiled the UK's future regulatory framework for fund managers.

The latest proposals from the Treasury and the FCA fundamentally revamp the UK's alternative investment fund managers (AIFM) regime and aim to reduce regulatory burdens while maintaining essential protections for consumers and market integrity.

EU legacy rules

UK fund managers are currently regulated by a set of legacy rules derived from the EU's Alternative Investment Fund Managers Directive (AIFMD). Despite Brexit, the UK's regulatory framework for fund managers has so far largely remained unchanged and continues to mirror AIFMD.

In April 2024, the EU passed updates to AIFMD known as "AIFMD II" that are set to come into effect in April 2026 and offer an evolution rather than revolution of existing regulation.

However, the UK government, instead of adopting rules similar to AIFMD II, has proposed fundamental changes to the current regulatory framework for private fund managers, emphasising deregulation to enhance business operations and drive economic growth. The Treasury's proposals aim to streamline the framework for UK AIFMs.

Treasury threshold changes

Currently, the regulatory framework that governs alternative investment fund managers (AIFMs) hinges on thresholds relating to their assets under management (AUM).

This is a one-size-fits-all regime that holds irrespective of what type of funds they managed and what intrinsic challenges and risks different funds types present.

Since their introduction more than a decade ago, the thresholds have remained unchanged, creating cliff-edge effects where market fluctuations can suddenly impose significant regulatory burdens on AIFMs.

FCA empowered

The Treasury's vision for the future of UK asset management is a regime that is more tailored to fund managers' different business models.

It wants to empower the FCA to set and adjust thresholds more dynamically based on firm size, activities and. The FCA has published its own "call for input" indicating how it intends to create this proportionate regulatory framework.

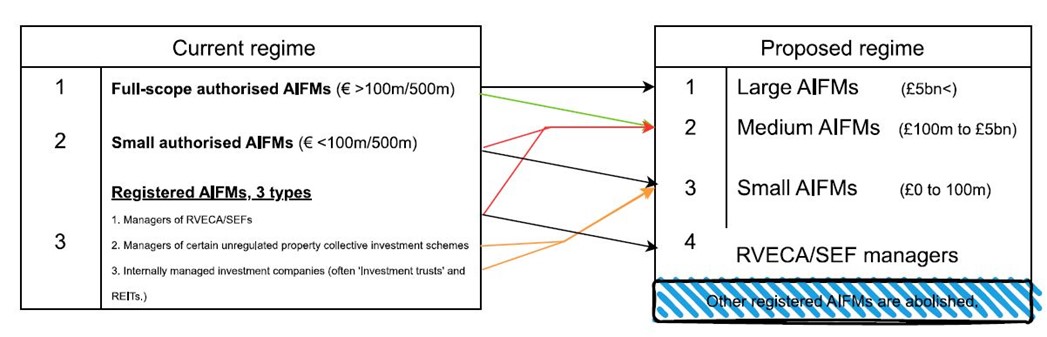

New AIFM taxonomy

The taxonomy that applies to AIFMs will look quite different. And thresholds will be calculated in a new manner too (see the impact assessment below).

The Treasury has suggested abolishing the registration regime for the smallest AIFMs, meaning they will all need authorisation from the FCA. The Treasury will consider separately how to address the regimes relating to managers of registered capital funds (RVECA) and social enterprise funds.

Each category of fund managers will have specific rules that reflect their operational scale and risk profile derived from both their AUM and the types of alternative funds they manage. Unnecessarily burdensome or prescriptive rules will be removed across the board, whereas some bespoke rules may only apply to firms doing specific activities.

The FCA has announced it will conduct a separate review of the operation and effectiveness of the prudential requirements, business restrictions, reporting regime and remuneration rules for AIFMs.

Other changes

Key definitions related to the regulatory perimeter would be transferred to the Regulated Activities Order for legal clarity.

The proposals include other legislative changes for the new regulatory framework. These include easing the requirement for a 20-day FCA notification before marketing AIFs and adjusting the disclosure of significant holdings in UK non-listed companies.

Additionally, concerns about external valuers' direct liability could be addressed by shifting to contractual liability, while the national private placement regime will remain unchanged.

Applicable thresholds

- Small AIFMs

Firms with an accumulated net asset value under management below £100million will adhere to core requirements appropriate to their size, risk profile and activity. This is in addition to the FCA's broader requirements such as the principles handbook.

- Midsize AIFMs

Firms with an accumulated net asset value under management between £100 million and £5 billion will be deemed mid-sized AIFMs and benefit from a more flexible and less prescriptive regime. The FCA also proposes adjusting the risk management requirements for mid-sized firms. Managers of funds that invest in non-transferable securities, such as private equity or real estate funds, may be subject to fewer risk management provisions.

The substance of a lot of the detailed procedural requirements currently in the AIFMD Level 2 Regulation will not apply moving towards an outcomes based regulation.

- Large AIFMs

Firms with an accumulated net asset value under management of £5billion and above, large AIFMs will continue to follow stringent regulations similar to the current full-scope regime but with reduced unnecessary burdens that will apply to all AIFMs.

- New regime's thresholds: impact assessment on UK AIFMs

Legend

Black: AIFMs not expected to be significantly impacted.

Red: AIFMs may change status from registered to authorised to mid-size AIFMs, with a potentially significant increase in regulatory burdens and compliance costs.

Amber: AIFMs may change status from small registered AIFMs to authorised AIFMs, with a potential increase in regulatory burdens and compliance costs.

Green: AIFMs likely to be subject to less regulatory burdens in addition to the cross-cutting deregulation.

Thresholds will be calculated in pound sterling not euro and in a simpler manner by reference to each AIFMs net asset value under management across the AIFs for which they have been appointed as an AIFM (without reference to leverage, which the EU's AIFMD is based on) to avoid complicated leveraged calculations. In practice, the same managers will be impacted under either calculation methods.Some of the details in the proposals are expected to change following the call for input, where they might otherwise go against the regulator's stated goal to "make the regime easier to understand and navigate, making it simpler for new entrants to join the market and for existing firms to grow without undue regulatory burdens".

Better tailored to UK investment managers

With the way UK fund managers are regulated set to fundamentally change, efficiencies may be harvested and new business opportunities should open for both UK and international fund managers. AIFMs, especially those operating in the mid-market segment, will benefit from following these developments closely, and consider how best to utilise the new framework.

The consultation and call for input closed for responses on 9 June. The FCA plans to publish detailed rules in the first half of 2026 together with an implementation timeline.

Osborne Clarke comment

We welcome the general direction of the new regime and especially the application of more proportionate thresholds and fewer detailed prescribed rules to AIFMs. We also welcome the tailoring of rules that recognises that a significant number of UK-based AIFMs are specialist boutiques, including the abolition of compliance burdens and regulatory obligations where they serve little purpose.

The lifting of the thresholds will have a significant impact. A 50-fold increase in the thresholds for full-scope AIFMs means a significant number of fund managers will be reclassified as mid-sized, and there is a real opportunity for these to experience a reduction in detailed and prescriptive requirements.

The drive to reducing procedural complexity and allowing firms greater flexibility in how they meet regulatory outcomes is most welcomed. That said the devil is in the detail. Outcomes-based rules can in practice replicate the regulatory burdens of full-scope AIFMs – even if procedurally lighter rules are in place – although this would depend on how they are implemented and how they interact with the FCA's broader requirements for authorised firms.

In a worst-case scenario, they could increase compliance complexity, risks and costs. We are concerned that the proposed regime for mid-sized fund managers by focusing on outcomes may not deliver proportionality in practice as it stands. We would like to see more detailed considerations put forward as to what rules are disapplied for different types of mid-size managers and, where compliance is required, to see the FCA issue guidance on what it will deem sufficient for or at least create an assumption of compliance. Alternatively, there is a risk that fund mangers will have to introduce detailed policies and procedures that effectively replicate the detailed "level 2" requirements.

There is also a risk of a disproportionate negative impact on some fund managers. Today, a large number of venture capital and private equity managers rely on a higher bespoke threshold (applying where they only manage unleveraged AIFs, and no investors have redemptions rights for five years following their initial investment). This increases the threshold for authorisation to €500 million from €100 million. As an equivalent threshold of say £1 billion net asset value has been omitted, these managers will have to adhere to the new "mid-size" authorisation rules, unless this is changed, meaning a significant uplift in regulatory burdens. We have specifically addressed this in our input to the regulator, as we hope this is an omission which will be changed.

For international investment managers with authorised firms in both the UK and EU the divergence between the two regimes might risk increasing compliance costs, including where there is delegation from an AIFM authorised in the EU to a UK investment manager, and they should consider carefully what they need to do to adhere to both regimes.

Osborne Clarke has responded to the call for input and has highlighted areas relevant for our clients that we think need to be addressed. If you would like help navigating the new UK asset management regime and assessing how it may impact or help your business, please contact our experts.