Life Sciences and Healthcare

A brave new world: UK real estate funds and the new non-resident capital gains tax on UK land

Published on 13th July 2021

April 2019 saw the introduction of a new regime taxing non-residents on gains on the direct and indirect disposal of interests in UK land and buildings. This new regime is the latest step in a series of changes over the past few years that have brought non-residents into the UK tax net (see our previous Insight for more on the background). The move reflects a desire by the UK tax authorities to have a level playing field between residents and non-residents.

What does it mean?

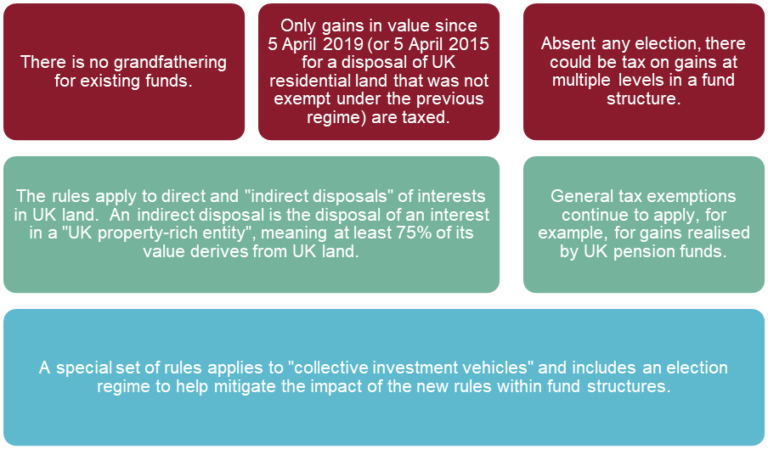

The new rules apply to non-resident individuals and other entities (such as companies or trusts) and impose UK tax on investment gains arising from a direct or indirect disposal of UK land and buildings on or after 6 April 2019. The rules apply to both commercial and residential land and replace the previous charging regime for certain non-UK residents holding UK residential land. The key points to note on the application of the new rules to fund structures are as follows:

Mitigation measures

When the proposals were announced, concerns were raised in the fund industry that the indirect disposals provisions would result in multiple layers of taxation for typical fund structures. The government listened and has introduced:- a special set of rules applying to Collective investment vehicles (CIVs) (as defined within the new rules and broadly made up of collective investments schemes, alternative investment funds, REITs and non-UK resident companies which are REIT like equivalents); and

- an election regime, the aim of which is to remove tax leakage within a fund structure, so that in many cases tax arises only at investor level and tax-exempt institutional investors are not prejudiced by the new rules.

What has not changed?

- These new rules only affect the tax treatment of capital gains. There is no change under the new rules to the tax treatment of income from UK land.

- The new rules do not change the tax treatment of partnerships, which are still treated as tax transparent for the purposes of chargeable gains.

- The new rules also do not change the position for UK tax resident investors, who remain liable to UK tax on all income and gains.

- All existing exemptions apply to gains arising, such as an exemption for qualifying pension funds, or sovereign exemptions.