Funds Legal Update | March 2021

Published on 4th March 2021

As a sign of the times, the key regulatory updates over the course of the last couple of weeks are exclusively environmental, social and governance (ESG) related

With 10 March 2021 scored into the diaries of many asset managers, the European supervisory authorities (ESAs) have provided guidance on their regulatory expectations around the Sustainable Finance Disclosure Regulation (SFDR) and the application date of the accompanying draft Regulatory Technical Standards (RTS). But when will the European Commission respond to the ESAs' five SFDR "priority issues"?

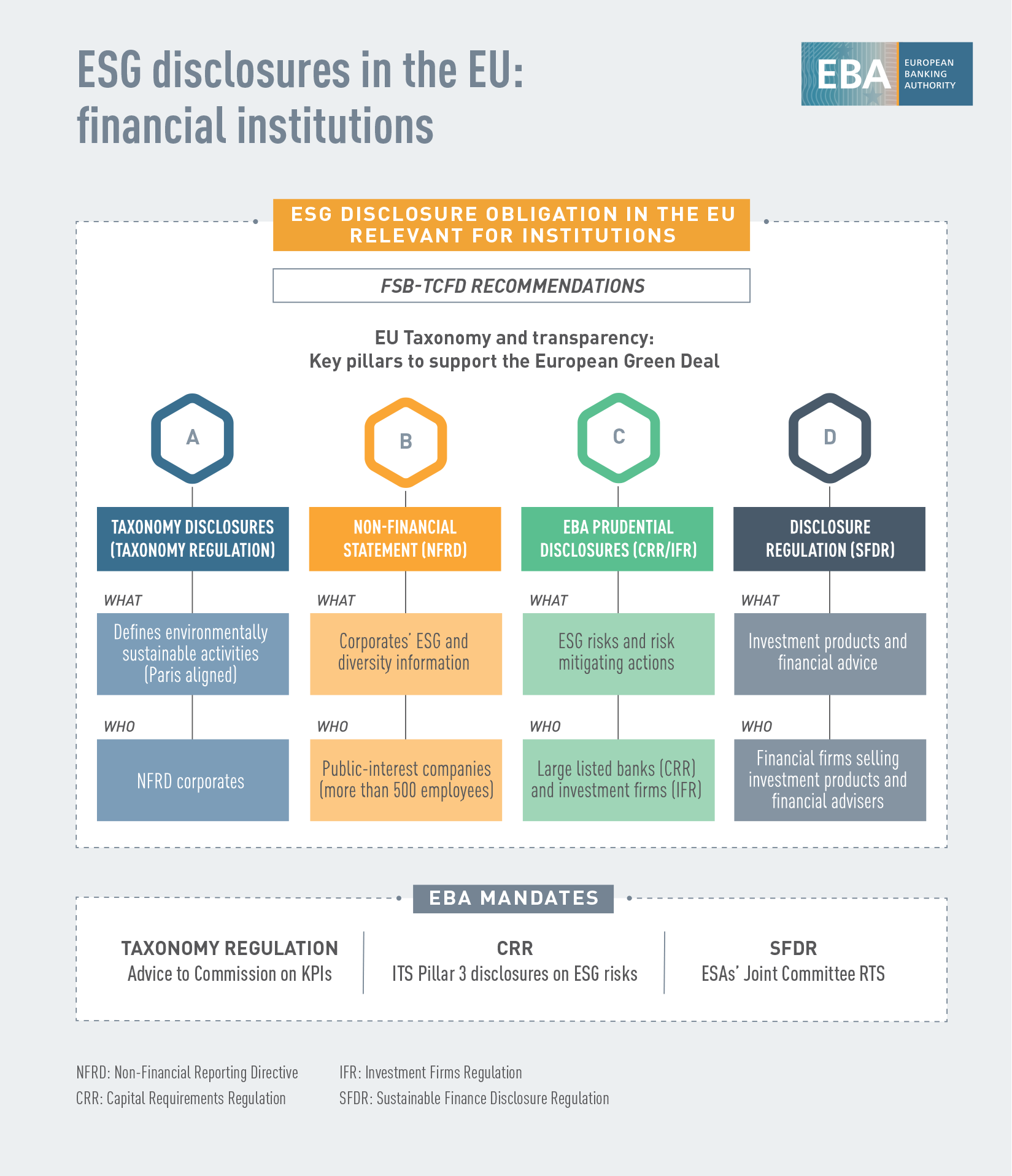

The ESAs have also published their advice on key performance indicators (KPIs) disclosing how, and to what extent, the activities of businesses that fall within the scope of the non-financial reporting directive (NFRD) qualify as environmentally sustainable under the EU Taxonomy Regulation.

Closer to home, the investment industry welcomes new best practice guidelines aimed at increasing diversity and inclusion across the sector, and we look at the new obligations for UK occupational pension schemes around climate risk governance and reporting duties.

ESAs confirm their regulatory expectations during the SFDR 'interim period'

Many of the substantive provisions under the SFDR kick-in on 10 March 2021. Yet, the accompanying RTS, which "plug the gap" in some of the SFDR's key areas (in particular with respect to detail on adverse impact reporting at entity level and the pre-contractual, website and periodic disclosures required from funds with an ESG focus), are unlikely to apply until 1 January 2022.

So should firms be referring to the draft RTS set out in the ESAs' Final Report (2 February 2021) with their respect to their compliance with the level one obligations under the SFDR?

The answer appears to be "yes". According to a joint supervisory statement published by the ESAs on 26 February 2021, the draft RTS should be used as a reference when applying the provisions of the SFDR in the interim period between the application of the SFDR (as of 10 March 2021) and the application of the RTS at a later date. Specifically, the statement provides that the draft RTS can be used as a reference for the purposes of applying the provisions of Articles 2a, 4, 8, 9, and 10 of the SFDR in that interim period.

While the ESAs have acknowledged the possibility that the final RTS adopted by the Commission may be different to the draft standards in their final report, they recommend that national competent authorities encourage in-scope firms to use the interim period from 10 March 2021 until 1 January 2022 to prepare for the application of the RTS.

Separately, the International Capital Market Association (ICMA) has published a note on the revised SFDR RTS. Those managers still struggling to categorise their products between article 6, 8 and 9 of SFDR may find some comfort in ICMA's view that this "may be an iterative process, as the consideration of KPIs and the implementation of DNSH ('do not significantly harm' principle) at product level are not yet well defined."

Finally, we are still waiting to see a response from the European Commission to the ESAs' letter (7 January 2020) seeking urgent clarification on five crucial areas of SFDR application ahead of the 10 March 2021 deadline.

Understanding the pathway towards sustainability and financing activities

What information should institutions subject to the NFRD disclose on how their financial or broader commercial activities align with economic activities identified as environmentally sustainable in the EU taxonomy?

This is the question that the European Banking Authority (EBA) (in respect of credit institutions and investment firms), the European Securities and Markets Authority (ESMA) (in respect of non-financial undertakings and asset managers) and the European Insurance and Occupational Pensions Authority (EIOPA) (in respect of insurers) have each addressed in their separate proposals published on 1 March 2021.

The summary below refers to the EBA and ESMA advice only. The EIOPA proposals are available here.

Non-financial undertakings and asset managers

ESMA's recommendations are set out in its Final Report on advice under Article 8 of the Taxonomy Regulation. They define the KPIs disclosing how, and to what extent, the activities of businesses within the scope of the NFRD qualify as environmentally sustainable under the Taxonomy Regulation. With respect to asset managers, the proposals set out the KPI that they should disclose, the methodology to be applied to that KPI and recommendations for the development of a coefficient methodology to assess the taxonomy-alignment of investments in investee companies that do not report under the NFRD.

ESMA also proposes that non-financial undertakings and asset managers use standardised templates for their reporting under Article 8 in order to facilitate comparability of these disclosures and enhance their accessibility to investors that will reuse this information.

Investment firms

Similarly, in the opinion and accompanying report and annexes, the EBA refers to the KPIs that institutions should disclose, on the scope and methodology for the calculation of those KPIs, and on the qualitative information they should provide. The main KPI proposed is the green asset ratio (GAR), which identifies the institutions’ assets financing activities that are environmentally sustainable according to the EU taxonomy, such as those consistent with the European Green Deal and the Paris agreement goals. Information on the GAR is supplemented by other KPIs that provide information on the taxonomy-alignment of institutions’ services other than lending and investing. The EBA has also integrated proportionality measures that should facilitate institutions’ disclosures, including transitional periods where disclosures in terms of estimates and proxies are allowed.

Finally, the EBA also makes a number of policy recommendations to support the reliability and comprehensiveness of institutions’ disclosures, including aiming for international standards and criteria to allow a better assessment of the taxonomy-alignment level of non-EU exposures and clients.

The number of different ESG initiatives being developed at an EU level which may impact asset management firms (including, in certain circumstances, UK managers) is significant. The EBA has developed this simple infographic setting out the four key pillars that support the European Green Deal, what the legislation is designed to achieve, and who it impacts.

Improving diversity and inclusion in the investment industry

On 12 February 2021, a number of leading venture capital and private equity investors published substantial guidelines on diversity and inclusion in the investment industry. The best practice guidelines are intended to help increase investment in under-represented founders and drive diversity and returns across the investment sector, and are aimed at investors who are beginning their diversity and inclusion journey as well as those who are further along the process.

The "Guidance and best practice examples for VCs, private equity and institutional investors" document was written by leading investors and professionals including Atomico, Pollen Street Capital, Ada Ventures, Adelpha, Astia, KPMG, Diversity VC and Diversio, with a focus on four areas:

- Talent acquisition, retention and development.

- Internal education, culture and policy.

- Outreach, access to deal flow, and unconscious investment bias.

- Influence, external guidance and portfolio management.

The document recommends that investors get certified under “The Standard” developed by Diversity VC, Diversio and OneTech, and undertake a portfolio assessment to ensure their funds are being allocated fairly and objectively. In addition, all financial organisations are encouraged to become signatories to the Investing in Women Code to support the advancement of female entrepreneurship in the UK by improving access to tools, resources and finance from the financial services sector.

Climate risk governance and reporting duties: new obligations for occupational pension schemes

The Pension Schemes Act received Royal Assent on 11 February 2021. In the first of a series of Insights on the changes being made by the Act, we look at what new climate risk duties mean for trustees and employers. See our Insight on this here.

{kind=link}