Failure to prevent tax evasion: how will the new law affect recruitment businesses?

Published on 14th July 2017

- The new corporate offence is a Bribery Act style “failure to prevent” offence, with an unlimited fine and criminal record for corporations if convicted.

- Reasonable procedures to prevent the facilitation of tax evasion must be in place in order to establish a defence.

- All corporations irrespective of sector and size should take action now before the offence comes into force, on 30 September 2017.

- The staffing supply chain is under scrutiny by authorities in relation to things like offshore payment schemes, and some aggressive onshore schemes (such as the Anderson scheme reported on this month) and some aspects of false self-employment.

- Any recruitment/staffing business looking to sell will, as part the due diligence process, need to demonstrate that they have carried out a risk assessment and provided training to their staff about the offence.

This new offence follows in the wake of the Panama Papers and other high-profile tax scandals. Tax evasion and avoidance is a political hot topic and there appears to be broad public and cross-party support for increasing the powers of the state to combat evasion and financial crime in general.

The aim of the new offence is to make it much easier to convict corporates for the facilitation of tax evasion by their employees or associated persons. Like the Bribery Act 2010, it is a move to a US-style strict liability approach. Also like the Bribery Act, if a defence is to be established, the onus is on the corporate to demonstrate that it had reasonable procedures in place to prevent the prohibited conduct.

Whilst entities operating within the financial services sector that offer tax advice are the prime targets of the legislation, it is absolutely clear from HMRC guidance that all corporations are within scope, so all corporations should be taking steps to prepare for it. This will involve, at the very least and as a first step, adapting your wider financial crime compliance programme to include a specific tax evasion risk assessment, and acting on any areas identified as high-risk.

Overview of the new offence

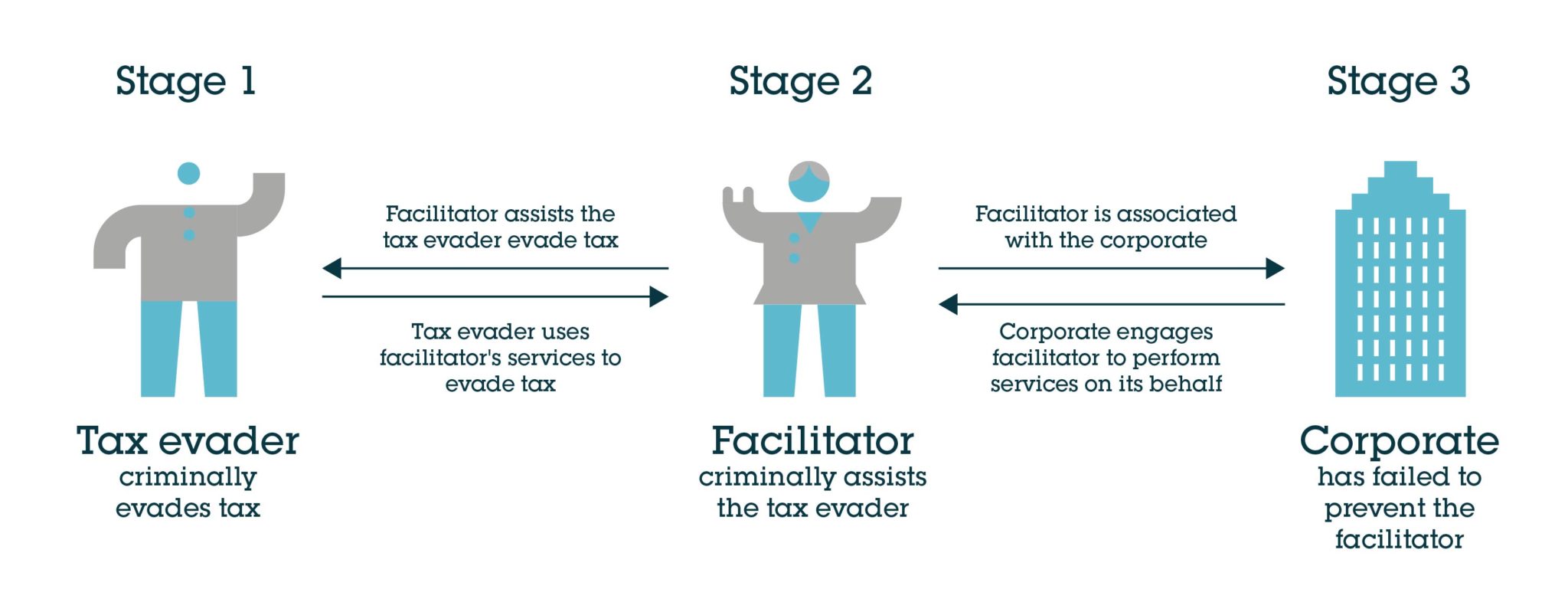

A corporation will be guilty of the new offence if all three steps below are established:

- a tax evasion offence is committed by a tax payer (a tax evader) (e.g. a contractor or local payroll company);

- the commissioning of that offence is criminally facilitated by a third party (the facilitator) (which might be a recruitment consultant who has made a recommendation); and

- the facilitator is associated with the corporation (the recruitment consultant’s employer).

It is important to note that criminal intent on the part of both the tax evader and the facilitator must be established. There are, therefore, two underlying criminal offences that must be committed in order to hold the corporation liable, although it is not necessary for the offences to be prosecuted or the perpetrators convicted. However there is no requirement to establish intent on the part of the corporate. In fact, the corporate can be convicted even if it did not benefit from the offence.

This perhaps opens the door for prosecuting authorities to make deals with evaders and facilitators in order to go after the higher-profile and deeper-pocketed corporates. The legislation is not designed to capture the misuse of legitimate services that are provided in good faith. However, looking at the UK staffing industry, there will be situations where the “solution” is offered and bought on the understanding that tax will be minimised or reduced and in some cases that may create problems and potential liabilities under the new legislation. This is the area that will require some attention, particularly if preparing for sale.

Tax evasion or tax avoidance, and how does this affect staffing and recruitment companies?

The question as to where the line is drawn between criminal tax evasion/facilitation and legitimate tax avoidance is an uncertain one. It is important to note that the new offence does not address this question.

However, based on a perceived shift in public opinion and the new weapon in their armoury in the form of the corporate offence following recent tax scandals, it is possible that prosecutors will be emboldened in terms of the where they draw the line between avoidance and evasion or “cheating the revenue”. This could result in an increase in prosecutions.

This is of importance to staffing businesses and their recruitment consultants involved in referring contract workers to payment “solutions” involving tax avoidance arrangements. It is now perhaps less clear whether “solutions” designed to use tax legislation to provide outcomes not intended by Parliament, will fall the right side of the line.

According to the guidance, where a person makes an introduction in good faith, and believes the external service provider is unlikely to be involved in facilitating tax evasion, and also steps away from the transaction entirely, the company which makes the referral is unlikely to fall within scope of the new offence. However, this would not be the case where the introducing party is aware that either the motive of the contractor/temp involved is to evade tax or that the external provider to whom a contractor/temp has been introduced is likely to be involved in facilitating tax evasion. This dishonest referral would itself constitute a deliberate action to facilitate tax evasion at the taxpayer level.

It will, therefore, become increasingly important to recruitment businesses to carry out effective supply chain checks and to monitor referrals made to third party paying companies by their recruitment consultants.

In any event, the receipt by a recruitment consultant of a “kick-back” payment (whether in monetary or other form) which goes undeclared for tax and NI purposes will, almost certainly constitute criminal tax evasion, and may be seen as aggravating any offence relating to whatever referral the kick back was for. Their employers will be liable in each case. We recommend employers to carry out a thorough compliance exercise in order to put themselves in the strongest position from a proportionate procedures defence point of view.

It is also worth noting that the guidance states that some sectors pose a higher risk of facilitating tax evasion than others. These include tax advisory sectors: i.e. sectors in which providers of tax reducing payment “solutions” operate. Andersen is one such “advisor” which, according to recent reports, has closed its small umbrella businesses following HMRC scrutiny of its tax avoidance schemes.

Who is an associated person?

Corporations will only commit the new offence if the facilitation offence was carried out by an associated person.

The definition of an associated person, though, is deliberately broad. It includes employees, agents and anyone who performs services for and on behalf of the corporate (which could include distributors, subcontractors, consultants, joint venture partners, subsidiaries and other group companies). In other words it could conceivably apply to people to whom a staffing company has outsourced compliance or payroll activities.

For large corporations with extensive global networks this could amount to hundreds of entities.

Territorial scope

The territorial scope is extremely wide, with the new legislation comprising two separate offences: a UK tax evasion offence and a foreign tax evasion offence.

With the UK tax evasion offence, the tax evader must be a UK tax payer, but the corporation can be from anywhere in the world and needs no UK nexus in order to be guilty of the corporate offence.

With the foreign tax evasion offence, the tax evader must have committed a tax evasion offence in the country in question, but the conduct must also amount to an offence in the UK. The facilitator must also have committed a facilitation offence in the country in question, which must also be a facilitation offence in the UK. Unlike the UK offence, the corporate must have some connection with the UK in order to be brought within the scope of the foreign tax evasion offence, but this could be as remote as part of the facilitation being carried out in the UK.

How can a corporation establish a defence?

As the offence is a strict liability offence, if stages one and two are committed then the relevant body will have committed the new corporate offence unless it can show it has put in place reasonable preventative procedures.

Once the underlying offences have been proven (but, as referred to above, not necessarily prosecuted), the burden shifts to the corporation to show it had reasonable and proportionate procedures in place to prevent the facilitator doing what he or she did.

As with the Bribery Act, the legislation and supporting guidance takes a principle-based approach. There are 6 “guiding principles”:

- risk assessment;

- proportionality of risk-based prevention procedures;

- top-level commitment;

- due diligence;

- communication (including training); and

- monitoring and review.

What is reasonable and proportionate for a corporate will depend entirely on the circumstances particular to it. Corporations will need bespoke procedures based on an assessment of the particular risks it faces. Upon carrying out a risk assessment, it may be reasonable and proportionate for a corporation to conclude that a light touch compliance regime is required, but it is vital as an absolute minimum requirement that a risk assessment is carried out, documented and regularly reviewed.

Practical example (based on guidance published by HMRC):

A UK manufacturer contracts with a distributor to sell its products. Unknown to the manufacture, the distributor facilitates a VAT invoicing fraud enabling the distributor’s customer to evade VAT in the UK.

In this example, the manufacturer is liable for failing to prevent the facilitation of tax evasion by the distributor, unless it can demonstrate it had reasonable procedures in place to prevent the facilitation offence.

Based on the guidance from HMRC, the manufacturer is low to medium risk as far as its facilitating tax evasion risk profile is concerned, which will affect the level of procedures that is needs to have in place. The guidance indicates that a reasonable procedures defence is likely to be established if the manufacturer carried out a tax evasion facilitation risk assessment, implemented policies and procedures to mitigate identified risks and carried out a due diligence assessment of the distributor. The guidance suggests that carrying out due diligence further down the supply chain than the distributor would be disproportionate.

For higher risk corporations, such as entities that operate in the financial services sector (and in particular tax advisory firms) and/or high risk jurisdictions (such as tax havens), a much more rigorous compliance regime will be required in order to establish the defence.

It is also worth noting that HMRC expects that a feature of any compliance regime will be timely self-reporting following the discovery of a suspected facilitation offence being carried out by an associated person.

HMRC guidance is clear that it will expect corporations to have at the very least carried out a tax evasion facilitation risk assessment and be working towards implementing a bespoke set of reasonable and proportionate procedures by the time the legislation is in force, expected to be autumn 2017.

If your corporation has not already done so, we recommend taking action now to start this process. We can work with you to understand what this might involve, and how you can integrate your compliance and reporting programmes to future-proof against the current trend of ever-increasing levels of corporate transparency and liability.

We recommend that all recruitment and staffing companies act now to start this process.