Failure to prevent tax evasion: are you prepared for the new corporate offence?

Published on 31st March 2017

- The new corporate offence is a Bribery Act style “failure to prevent” offence, with an unlimited fine and criminal record for corporations if convicted.

- Reasonable procedures to prevent the facilitation of tax evasion must be in place in order to establish a defence.

- All corporations irrespective of sector and size should take action now before the offence comes into force (expected to be this Autumn).

In our June 2016 insight, we highlighted the new corporate offence of failing to prevent the criminal facilitation of tax evasion. Back then, the proposed offence was at the consultation stage. Fast forward 9 months, it is making rapid progress through parliament as part of the Criminal Finances Bill and is likely to come into force this Autumn.

This new offence follows in the wake of the Panama Papers and other high-profile tax scandals. Tax evasion and avoidance is a political hot topic and there appears to be broad public and cross-party support for increasing the powers of the state to combat evasion and financial crime in general.

The aim of the new offence is to make it much easier to convict corporates for the facilitation of tax evasion by their employees or associated persons. Like the Bribery Act 2010, it is a move to a US-style strict liability approach. Also like the Bribery Act, if a defence is to be established, the onus is on the corporate to demonstrate that it had reasonable procedures in place to prevent the prohibited conduct.

Whilst entities operating within the financial services sector that offer tax advice are the prime targets of the legislation, it is absolutely clear from HMRC guidance that all corporations are within scope, so all corporations should be taking steps to prepare for it. This will involve, at the very least and as a first step, adapting your wider financial crime compliance programme to include a specific tax evasion risk assessment, and acting on any areas identified as high-risk.

Overview of the new offence

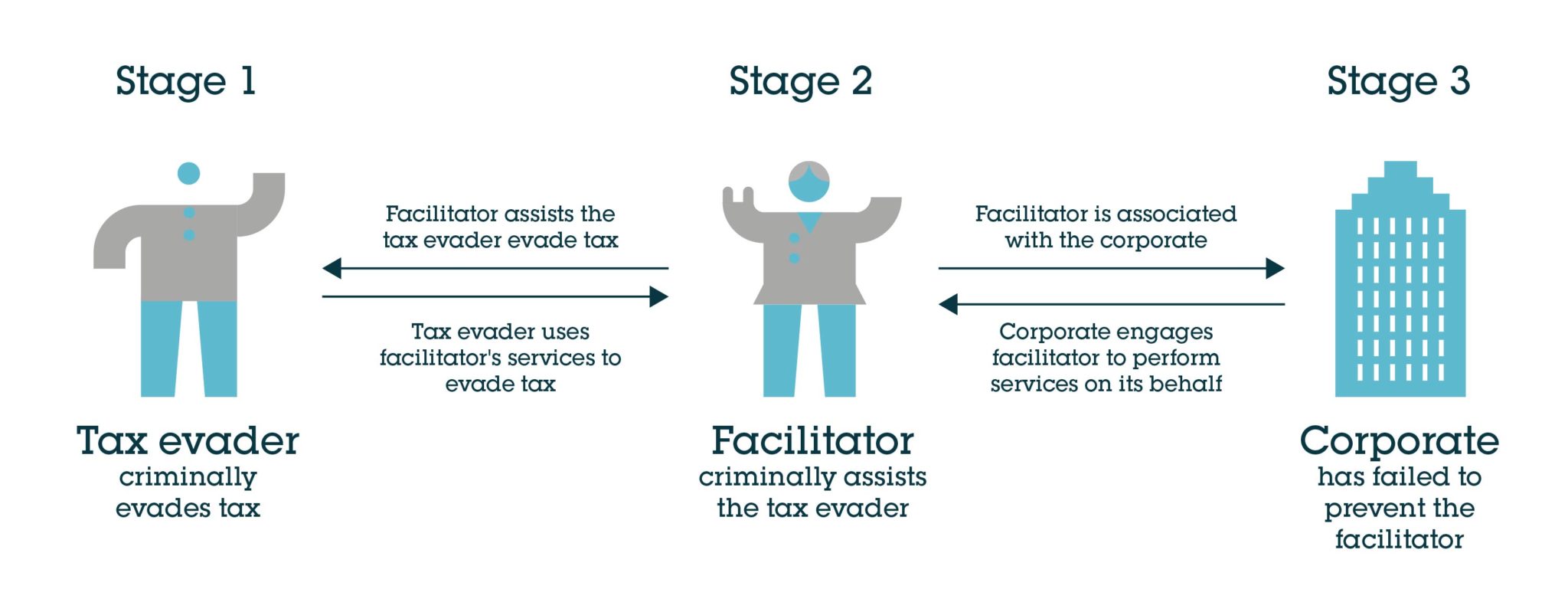

A corporation will be guilty of the new offence if all three steps below are established:

- a tax evasion offence is committed by a tax payer (a tax evader);

- the commissioning of that offence is criminally facilitated by a third party (the facilitator); and

- the facilitator is associated with the corporation.

It is important to note that criminal intent on the part of both the tax evader and the facilitator must be established. There are, therefore, two underlying criminal offences that must be committed in order to hold the corporation liable, although it is not necessary for the offences to be prosecuted or the perpetrators convicted. There is also no requirement to establish intent on the part of the corporate. In fact, the corporate can be convicted even if it did not benefit from the offence.

This perhaps opens the door for prosecuting authorities to make deals with evaders and facilitators in order to go after the higher-profile and deeper-pocketed corporates. It is also anticipated that the new offence will offer prosecuting authorities further opportunity to deploy the much-heralded, but as yet sparingly used, deferred prosecution agreement as a tool to encourage corporations to self-report and avoid criminal conviction.

Who is an associated person?

Corporations will only commit the new offence if the facilitation offence was carried out by an associated person.

The definition of an associated person, though, is deliberately broad. It includes employees, agents and anyone who performs services for and on behalf of the corporate (which could include distributors, subcontractors, consultants, joint venture partners, subsidiaries and other group companies).

For large corporations with extensive global networks this could amount to hundreds of entities.

Territorial scope

The territorial scope is extremely wide, with the new legislation comprising two separate offences: a UK tax evasion offence and a foreign tax evasion offence.

- With the UK tax evasion offence, the tax evader must be a UK tax payer, but the corporation can be from anywhere in the world and needs no UK nexus in order to be guilty of the corporate offence.

- With the foreign tax evasion offence, the tax evader must have committed a tax evasion offence in the country in question, but the conduct must also amount to an offence in the UK. The facilitator must also have committed a facilitation offence in the country in question, which must also be a facilitation offence in the UK. Unlike the UK offence, the corporate must have some connection with the UK in order to be brought within the scope of the foreign tax evasion offence, but this could be as remote as part of the facilitation being carried out in the UK.

How can a corporation establish a defence?

Once the underlying offences have been proven (but, as referred to above, not necessarily prosecuted), the burden shifts to the corporation to show it had reasonable and proportionate procedures in place to prevent the facilitator doing what he or she did.

As with the Bribery Act, the legislation and supporting guidance takes a principle-based approach. There are 6 “guiding principles”:

- risk assessment;

- proportionality of risk-based prevention procedures;

- top-level commitment;

- due diligence;

- communication (including training); and

- monitoring and review.

What is reasonable and proportionate for a corporate will depend entirely on the circumstances particular to it. Corporations will need bespoke procedures based on an assessment of the particular risks it faces. Upon carrying out a risk assessment, it may be reasonable and proportionate for a corporation to conclude that a light touch compliance regime is required, but it is vital as an absolute minimum requirement that a risk assessment is carried out, documented and regularly reviewed.

| Practical example (based on guidance published by HMRC):

A UK manufacturer contracts with a distributor to sell its products. Unknown to the manufacture, the distributor facilitates a VAT invoicing fraud enabling the distributor’s customer to evade VAT in the UK.

In this example, the manufacturer is liable for failing to prevent the facilitation of tax evasion by the distributor, unless it can demonstrate it had reasonable procedures in place to prevent the facilitation offence.

Based on the guidance from HMRC, the manufacturer is low to medium risk as far as its facilitating tax evasion risk profile is concerned, which will affect the level of procedures that is needs to have in place. The guidance indicates that a reasonable procedures defence is likely to be established if the manufacturer carried out a tax evasion facilitation risk assessment, implemented policies and procedures to mitigate identified risks and carried out a due diligence assessment of the distributor. The guidance suggests that carrying out due diligence further down the supply chain than the distributor would be disproportionate. |

For higher risk corporations, such as entities that operate in the financial services sector (and in particular tax advisory firms) and/or high risk jurisdictions (such as tax havens), a much more rigorous compliance regime will be required in order to establish the defence.

It is also worth noting that HMRC expects that a feature of any compliance regime will be timely self-reporting following the discovery of a suspected facilitation offence being carried out by an associated person.

HMRC guidance is clear that it will expect corporations to have at the very least carried out a tax evasion facilitation risk assessment and be working towards implementing a bespoke set of reasonable and proportionate procedures by the time the legislation is in force, expected to be Autumn 2017.

If your corporation has not already done so, we recommend taking action now to start this process. We can work with you to understand what this might involve, and how you can integrate your compliance and reporting programmes to future-proof against the current trend of ever-increasing levels of corporate transparency and liability.

We recommend that all corporations act now to start this process.