COVID-19: Compliance Risk Survey 2020

Published on 20th July 2020

| Download > |

COVID-19 will have a lasting impact on the way businesses approach compliance. Less than a quarter believe that their compliance systems are as effective as they need to be. Where businesses do get compliance right, the financial return can be significant.

Our report is based on an independent survey, conducted by Censuswide in June 2020, with a sample of 101 respondents who are decision makers over their company's corporate legal compliance processes and budgets in the UK or across multiple jurisdictions. The report explores the impact of the coronavirus pandemic on how businesses are now perceiving compliance risks, their approach to compliance and changes to investment in compliance. How does your business compare and how will you invest in legal compliance over the next 5 years?

- Foreword

- Executive summary

- Section 1: COVID-19 impact on budgets and future spend

- Section 2: COVID-19 impact on risk areas

- Section 3: Measuring effectiveness

- Section 4: Barriers and impact on future investment

- Conclusion

- Our Global Compliance service

Foreword

Businesses face greater amounts of regulation than ever before and increasing fine levels. Consequently, corporate legal compliance and risk management have become increasingly important. Focusing on, thinking about and managing compliance are now part of how a company operates. As Paul McNulty, the former US Deputy Attorney General, once noted: "if you think compliance is expensive, then you should try non-compliance".

What we wanted to discover, as part of this research, is how businesses are spending their legal compliance budgets and how they are measuring the return on investment. We also wanted to understand what impact the coronavirus would have on how businesses approach compliance. The results are striking: 56% agreed*** that COVID-19 would result in a permanent increase in compliance risk. However, the respondents were split equally on whether COVID-19 would result in an increase**** (51%) or decrease**** (49%) in investment in legal compliance next year. Companies with a turnover of £100 million or more expected a decrease; companies with a turnover of less than £100 million anticipated an increase. When the period was extended to the next five years, more than 70% expected an increase. Despite short-term uncertainty, respondents anticipated that increased compliance spend would return in the longer term.

Health and safety and cybersecurity were seen as posing the greatest increased risk as a result of COVID-19, and around two-thirds of respondents are anticipating increased investment in supply chain management and emphasis on environmental, social and governance (ESG) issues.

There is a marked difference in perception between the Board/C-suite and those in legal/compliance roles; more Board/C-suite members than legal/compliance officers agreed*** that COVID-19 will result in a permanent increase in compliance risk (63% and 50% respectively). This may simply be due to the legal/compliance respondents being closer to the detail of how compliance risks are already controlled. However, it’s clear that there’s a gap in understanding that legal/compliance roles need to address with their Boards.

Compliance processes and procedures should, of course, be effective and it is good to see that 86% of respondents measure the effectiveness of their legal compliance programmes. Auditing was cited by 63% as the most used measure, closely followed by whistle-blowing complaints (61%). The majority of respondents (54%) based their measure of financial return on whether regulatory fines have been imposed. These measures are relevant. However, it would be good to see businesses measuring the effectiveness of their compliance systems with more pro-active and leading indicators: for example, through the greater use of employee surveys and increased productivity. 15% of the respondents estimated a financial return of between £1 million and £10 million, as a result of their corporate legal compliance programme.

What about future trends? Businesses have indicated that investment will be driven by risks to reputation and where an ethical stance has been taken. These factors are seen as far more important than a fine imposed following a breach of regulation. However, aside from budget constraints, the greatest barrier to investing in legal compliance is the likelihood of enforcement by regulators. This suggests that a business is unlikely to invest in compliance if it perceives the risk of enforcement as low. Despite the very clear impact of COVID-19, the respondents were clear that technology would have the single biggest impact on investment in compliance over the next five years.

I hope you enjoy reading our report, and thanks to Censuswide for its independent administration of the survey. The Global Compliance Team at Osborne Clarke looks forward to helping our clients navigate the legal compliance challenges that lie ahead.

Katie Vickery, Co-Head of Global Compliance, Osborne Clarke

Executive summary

Download the full summary

Download the full summary

Section 1: COVID-19 impact on budgets and future spend

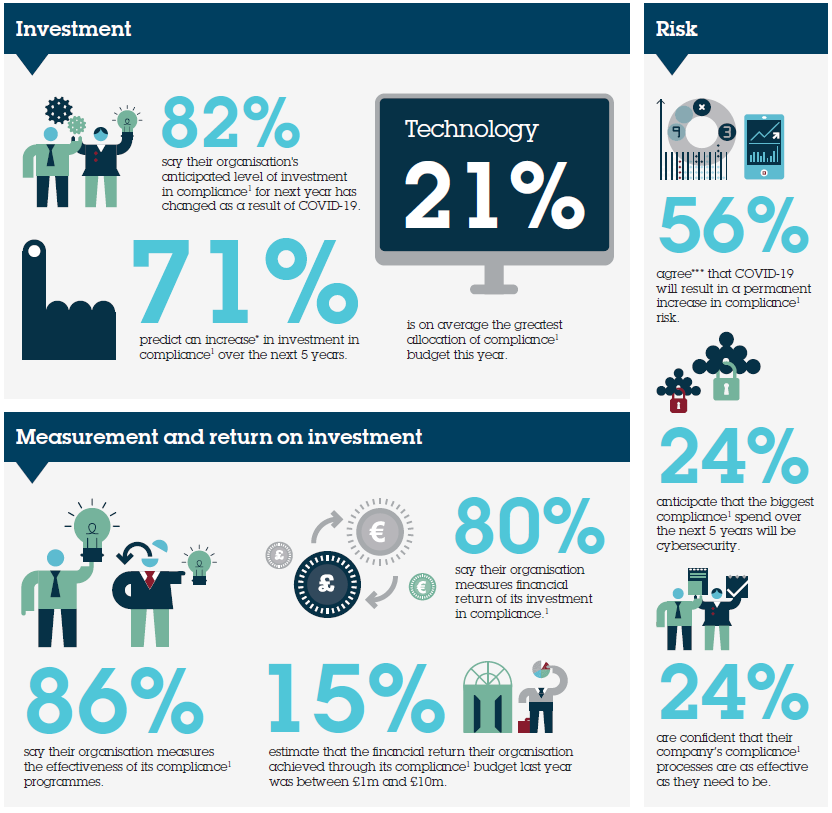

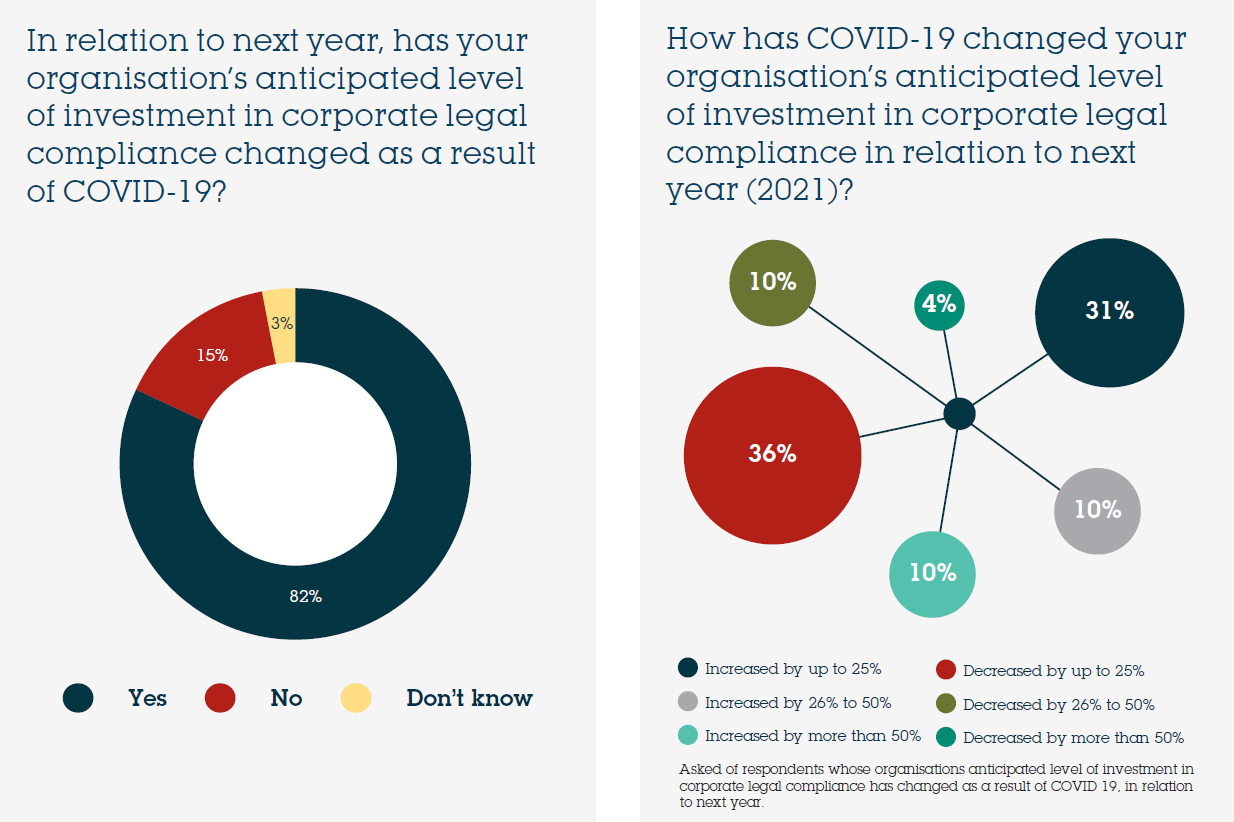

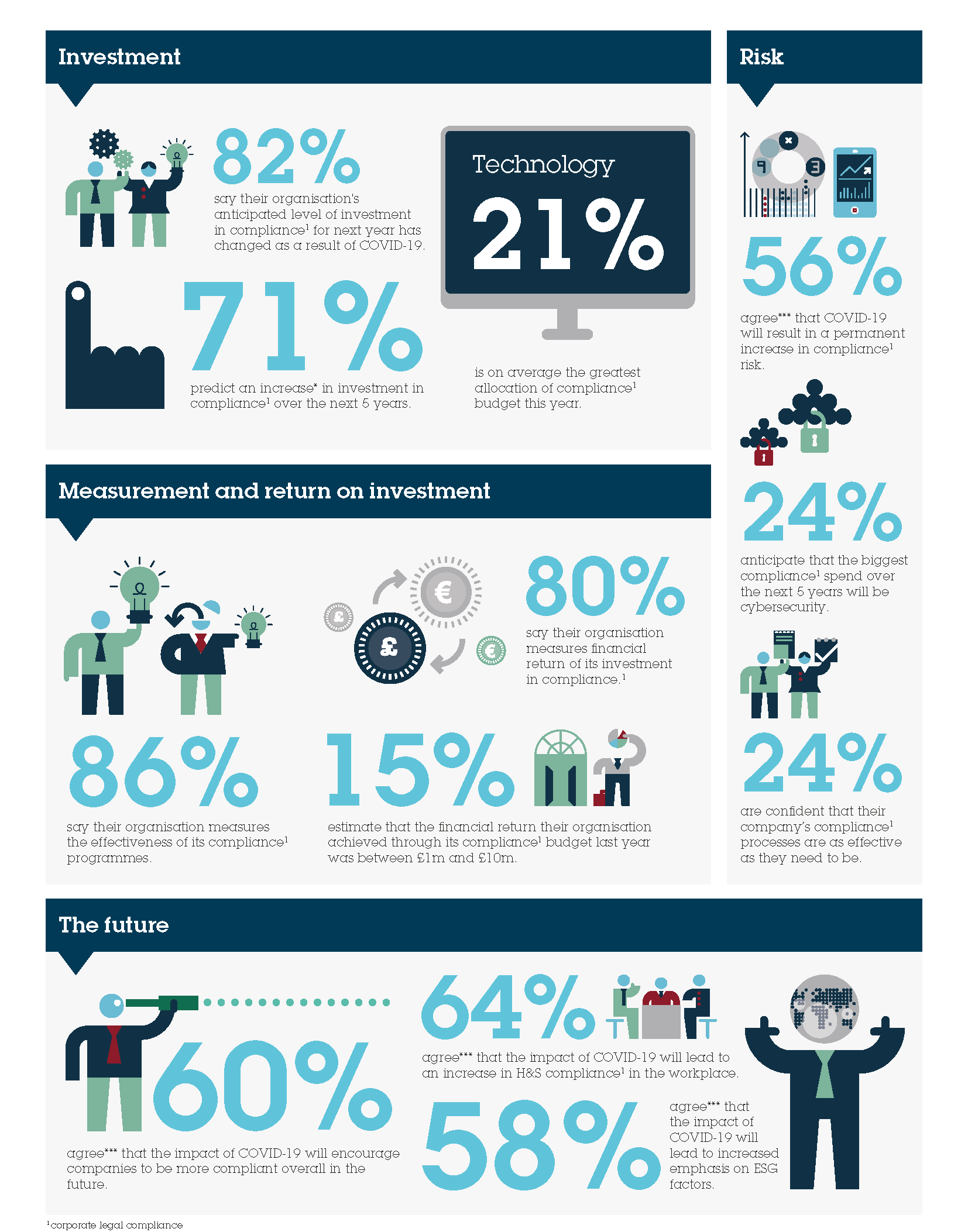

82% said their organisation’s anticipated level of investment in corporate legal compliance for next year has changed as a result of COVID-19.

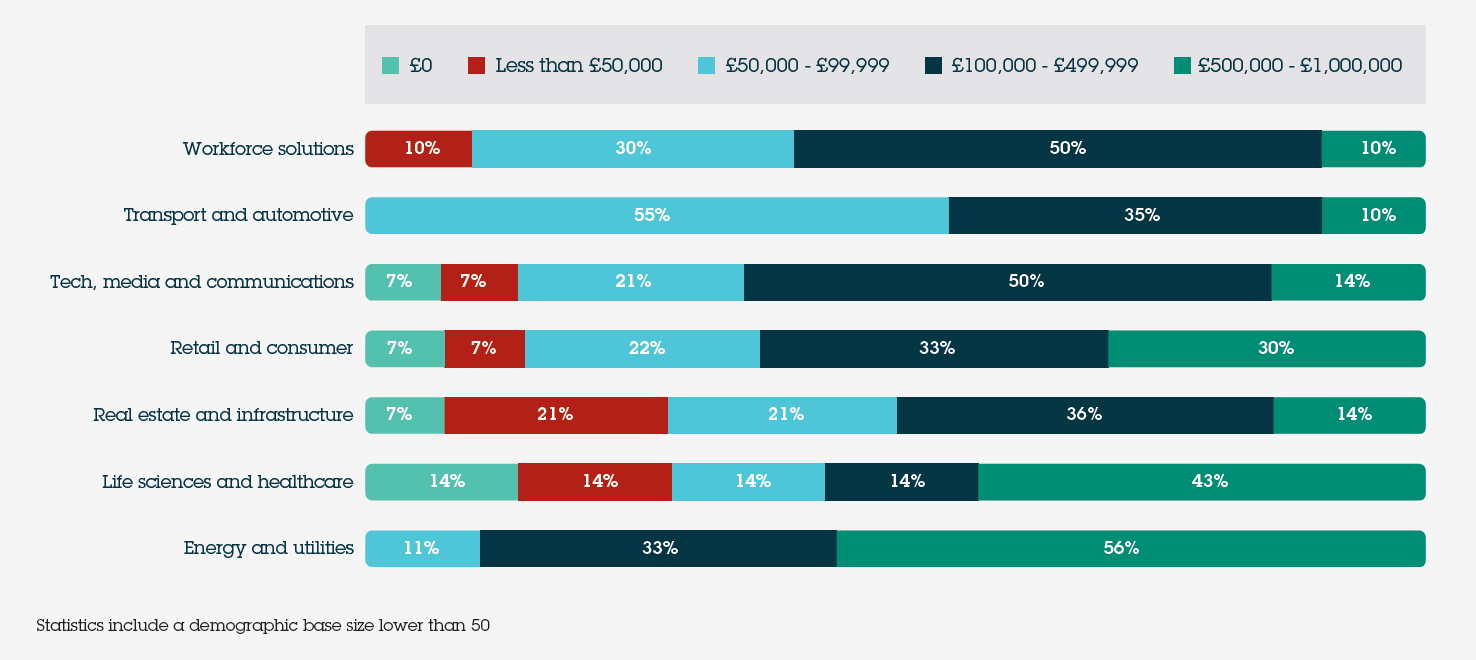

When your organisation’s budget was allocated this year, how much was allocated to corporate legal compliance (2020)? (Tick one)

Investment levels vary by industry and size

Almost 3 in 5 (59%) respondents said that £100,000 - £1,000,000 was allocated to corporate legal compliance in their budget allocation this year (2020). None of the respondents said that more than £1,000,000 was allocated to corporate legal compliance. However, telling differences emerge when the budgeting for compliance is broken down by sector. Given the nature of the sectors and potential consequences of non-compliance, it is unsurprising that in both life sciences and healthcare and energy and utilities, between 40%² and 60%² allocated over £500,000 to compliance. What is more surprising, and concerning, is how little is being spent by some businesses in the retail and consumer, technology, media and communications and real estate and infrastructure sectors. In particular, 7%² of respondents in each of those sectors are not spending anything on compliance. That is despite compliance being something that could fundamentally affect how (and if) a business operates. For businesses with a turnover of more than £100 million, only 1% or less of their turnover is being spent on compliance. Perhaps more concerning, 10% of businesses with a turnover of under £100 million are not spending anything towards achieving compliance.

²Statistics include a demographic base size lower than 50

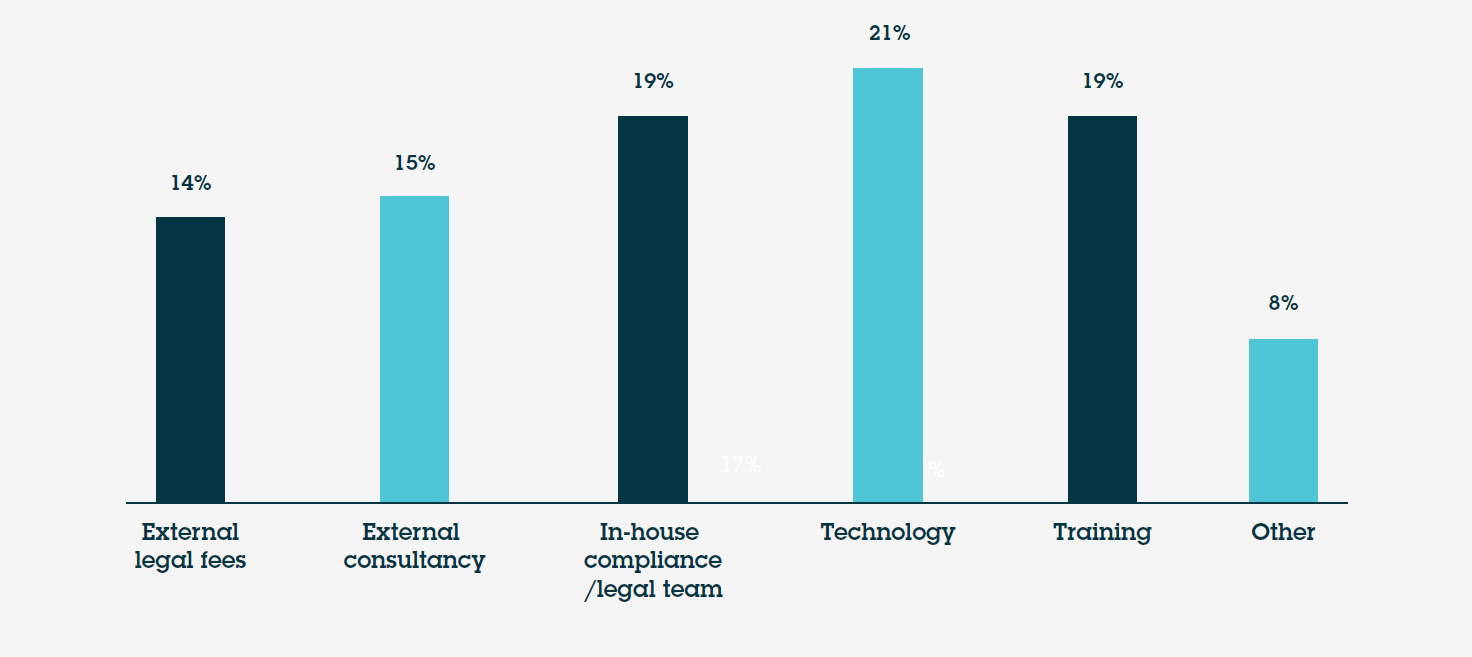

To the best of your knowledge, of your allocated corporate legal compliance budget, roughly what is the percentage split across the following areas?

Compliance experts utilising technology

The corporate legal compliance budget becomes more interesting when you delve into where and how it is being allocated. For example, the highest average percentage (21%) is allocated to technology, with 6% of respondents whose organisation allocated some of its budget to corporate legal compliance confirming that as much as between 41-50% of their budget is spent this way. This is perhaps indicative of the increase in compliance software that is available and businesses turning to automation to help implement compliance processes. Training remains a significant part of compliance spend, with an average of 19%, and just over a third of respondents (35%) noting that their organisation allocates between 21 and 30% of their budget on this. Although an average of 19% of budget is spent on in-house compliance, that is, perhaps, quite a low investment in the team of people who know your business best and should be at the forefront of driving improvements to your compliance systems.

| "It’s quite possible that these teams feel that they have the right people and the right processes in place and are now ready to make the technology investments to deliver the best outcomes,” explains Katie Vickery, Partner, Osborne Clarke. “Automating processes, which also combine compliance requirements, can deliver efficiencies for a business and achieve greater compliance in a way that does not feel overly burdensome. However, there is a risk that investing in technology is seen as a quick fix, where improving culture and process is much harder. But software can give a misplaced sense of confidence if the culture and processes are not in place to ensure it works effectively.” |

Investment set to increase over the next five years

Over 4 in 5 (82%) respondents said that their organisation’s anticipated level of investment in corporate legal compliance over the next year has changed as a result of COVID-19. Notably, for those with a company turnover of £100 million and more, this rose to 100% and for companies with a turnover of less than £100 million, this decreased to less than two-thirds (65%). When comparing Board/C-suite and legal/compliance, more respondents in legal/compliance roles (94%) expected their organisation’s level of investment in corporate legal compliance to change as a result of COVID-19 compared to those in Board/C-suite roles (71%). This may indicate to those in legal/compliance roles the importance of aligning the expectations of the Board/C-suite of the impact of coronavirus on compliance spend.

But what change are these respondents anticipating? Interestingly, the figures for increasing versus decreasing investment in corporate legal compliance for next year because of COVID-19 are very similar. Just over half (51%) of respondents whose organisations’ anticipated level of investment in corporate legal compliance in relation to next year has changed as a result of COVID-19 anticipate an increase**** in investment, while 49% anticipate a decrease.***** What is even more interesting is that 70% of the smaller businesses in our survey (with a turnover of less than £100 million) anticipate an increase**** in their organisation’s level of investment. This neatly indicates the high level of uncertainty in how the weeks and months ahead will impact compliance. The reverse is true for the larger companies with a turnover of £100 million or more where the majority (62%) anticipate a decrease.*****

But looking further ahead, the picture changes. More than 7 in 10 (71%) respondents anticipate their organisation’s level of investment in corporate legal compliance will either slightly or significantly increase over the next five years, with a third (33%) predicting a significant increase.

| Katie Vickery continues, “It’s very telling how divisive this question has been. There are new and complex challenges arising as a result of the pandemic, and many businesses are working in constrained financial conditions. You would therefore expect the smaller companies to be decreasing their investment in this area but in fact the reverse is true, with larger companies decreasing investment. This may be because smaller companies have not invested enough in the past and now, feeling more exposed to risk, have decided that investment in compliance is a way to protect the business. With all the pressures that COVID-19 has brought on business nobody will want the added pressure of a regulatory investigation or enforcement action. However, taking a longer-term view, over 70% anticipate an increase in investment over the next five years.” |

Section 2: COVID-19 impact on risk areas

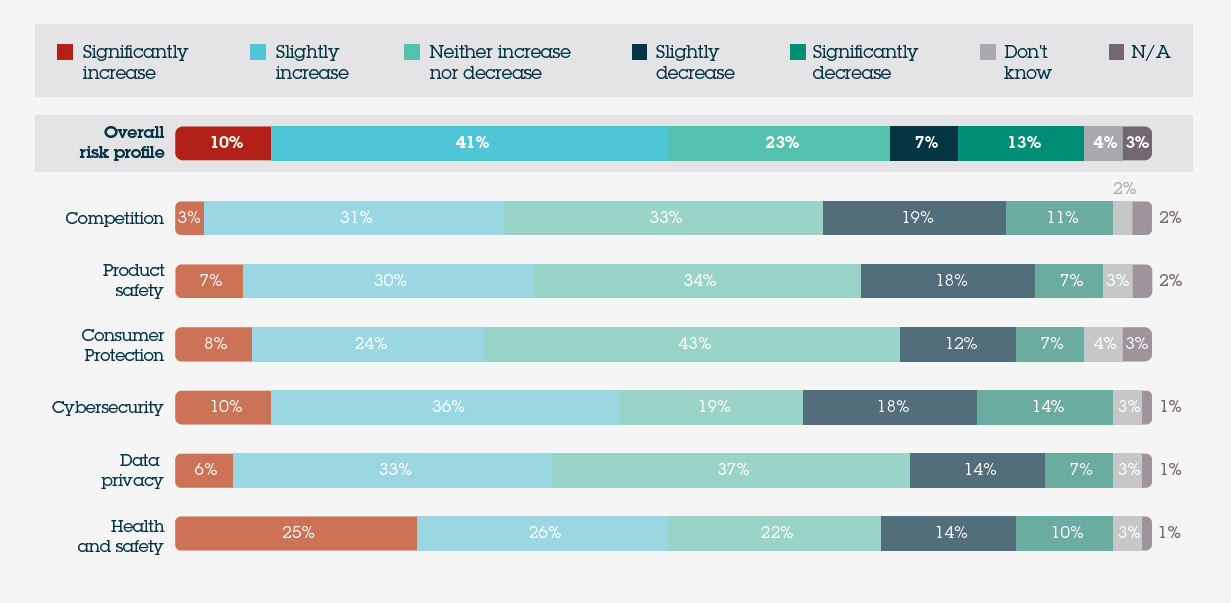

Over half of respondents anticipate that their overall risk profile will increase* as a result of COVID-19.

To what extent do you anticipate that the risk to your business will increase or decrease in the following areas, as a result of COVID-19?

Over half (51%) of respondents anticipate that their overall risk profile will increase* as a result of COVID-19. Respondents with a company turnover of £100 million and more generally expect more movement to their overall risk profile (whether that’s an increase or decrease) than those with a turnover of less than £100 million. For example, 41% of those with less than £100 million turnover expect an increase* of risk to their overall risk profile but this jumps to a more significant 60% for those with £100 million+.

Striking differences over health and safety risk

Given the way the pandemic has changed how employees will return to the workplace, using socially distant working arrangements, it’s perhaps no surprise that over half (51%) said they anticipate the health and safety risk to increase* as a result of COVID-19. However, it’s notable that almost a quarter (24%) think this will decrease.** There is a striking difference between the Board/C-suite respondents and those in legal/compliance-related roles, as almost 2 in 5 (38%) respondents with legal/compliance roles anticipate the health and safety risk to decrease** as a result of COVID-19, compared to just 1 in 10 (10%) of respondents in Board/C-suite roles.

| "COVID-19 has absolutely put a spotlight on health and safety compliance in the workplace. Businesses who previously perceived themselves as low risk, office environments for example, are now needing to dedicate significant resources and time to creating a COVID-secure working environment,” says Mary Lawrence, Partner, Osborne Clarke. “Those businesses that are anticipating a decrease could be because the effect of lockdown has demonstrated new ways of doing things, which actually presents less health and safety risk to the business.” |

Board/C-suite roles more concerned about cybersecurity risk

Many publications have reported on the cybersecurity risk that comes with remote working. This is a sentiment shared by businesses, as over 2 in 5 (46%) respondents think that the risk to cybersecurity will increase* due to COVID-19, compared to less than a third (32%) that think it will decrease.** A higher percentage of those at companies with a turnover of less than £100 million expect the cybersecurity risk to increase* than those with a turnover of £100 million+ (49% vs 42%) while 51% of respondents with Board/C-suite roles anticipate an increased* risk to cybersecurity, more so than those in legal/compliance roles (40%).

| "What’s encouraging here is how well IT and infosec teams have communicated their challenges to the Board. Board members now regularly state that cyber risk is their number one risk, with good reason. This is a real improvement from the position even a few years ago, when many IT and infosec teams were struggling to persuade their Boards to invest sufficiently in cybersecurity”, says Charlie Wedin, Partner, Osborne Clarke. |

A permanent increase in compliance risk

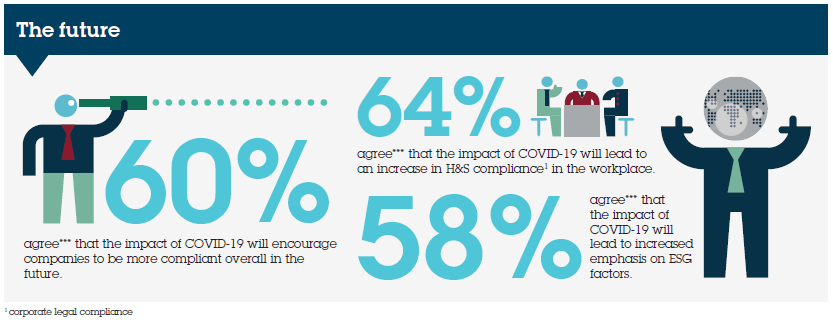

60% (3 in 5) of respondents agree*** that the impact of COVID-19 will encourage companies to be more compliant overall in the future. It’s worth noting that respondents with Board/C-suite roles agree with this more than those with legal/compliance roles (67% vs 54% respectively). Further, over half (56%) of respondents agree*** that the impact of COVID-19 will result in a permanent increase in compliance risk.

These two responses demonstrate the long-term impact on risk that COVID-19 has had and is having.

Increased investment in supply chain risk management

Focusing specifically on supply chains, over half (54%) of respondents agree*** that their organisation will spend more time on supply chain contingency planning and/or supply chain restructuring as a direct result of the impact of COVID-19.

For businesses with a company turnover of £100 million+, this increases to a much more substantial two-thirds (66%), whereas for those with a turnover of less than £100 million, this stands at 43%. This would seem to indicate that larger companies, which are likely to have more complex supply chains, have been more significantly impacted by COVID-19. Further to this, 3 in 5 (60%) respondents agree*** that the impact of COVID-19 will lead to increased investment in supply chain risk management. Once again, for those with company turnovers of £100 million or more, this rises to almost 7 in 10 (68%) compared to just over half (53%) for those with less than £100 million turnover.

| Will Robertson, Partner, Osborne Clarke, comments, “Very few businesses planned for the impact of world trade grinding to a halt so rapidly, or the huge dent left by supply chain malfunction. Now there’s focus on supply chains like never before and the genie is out of the bottle. It’s not just about building supply chains' back-up, but the realisation that international trade offers huge gains but also big risks. Contingency measures are required and many supply chains are tech-immature (and therefore quickly out of date and lagging). For the lawyers it’s also a reality hit that contractual management is often lacking, roles and responsibilities unclear, and the legal compliance matrix more complex than envisaged. Watch this space – supply chain risk management is clearly a hot focus area as this survey demonstrates.” |

ESG compliance

Almost 3 in 5 (58%) agree*** that the impact of COVID-19 will lead to an increased emphasis on environmental, social and governance (ESG) factors. This is truer for those with a company turnover of £100 million+ than those with a turnover of less than £100 million (64% vs 53%). In particular, 59% of respondents agree*** that decarbonisation will progress more in the next five years than it has done in the previous 20.

| "The role of ESG reporting and the wider drive for large corporates to implement net zero strategies, especially for larger businesses, is helping legal/compliance roles to drive conversations internally. The transparency that ESG brings in addition to the increased ESG scrutiny that corporates are facing – from a diverse range of stakeholders, including customers, employees, shareholders and funders – is a great way for compliance teams to push for change within an organisation and get more Board-level support and engagement,” says Matt Germain, Partner, Osborne Clarke. |

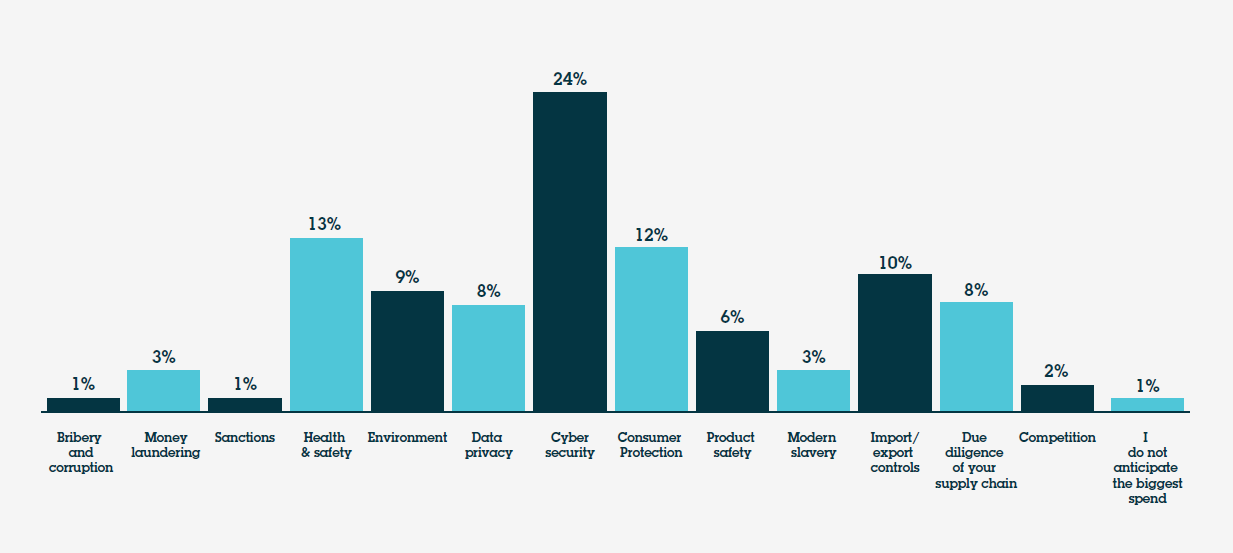

In which compliance area do you anticipate the biggest spend will be in your organisation over the next five years?

Health and safety

As previously suggested, COVID-19 will bring about significant change as people return to the workplace and this is echoed within the data. Just under two-thirds (64%) agree*** that the impact of COVID-19 will lead to an increase in health and safety compliance in their workplace. The stats remain high across company turnover comparisons as well as Board/C-suite and legal/compliance roles. However, when looking at spend, only 13% of respondents anticipated that health and safety would be their organisation’s biggest compliance spend in the next five years.

| "Health and safety compliance has been a key component of any corporate legal compliance programme for over 40 years now,” says Mary Lawrence. “It is not surprising that companies expect to spend less compared to the newer risk posed by cybersecurity. However, it is good to see businesses recognising the increased risk created by COVID-19 and that there needs to be some increase in spend accordingly.” |

Cybersecurity: biggest investment in next five years

The data revealed that over 2 in 5 (46%) respondents think that the risk to cybersecurity will increase* due to COVID-19 so it’s notable that almost a quarter of respondents (24%) anticipate that the biggest spend for compliance in their organisation over the next five years will be cybersecurity. Indeed, this was the highest percentage of all the areas of compliance.

| "This is reflective of risk and reality in the market,” says Charlie Wedin. “We have seen a material increase in cyber-attacks since COVID-19 forced many organisations into mass home-working – criminal attackers have been leveraging this seismic shift to seek financial gain from targeting vulnerable people and remote working systems.” |

Section 3: Measuring effectiveness

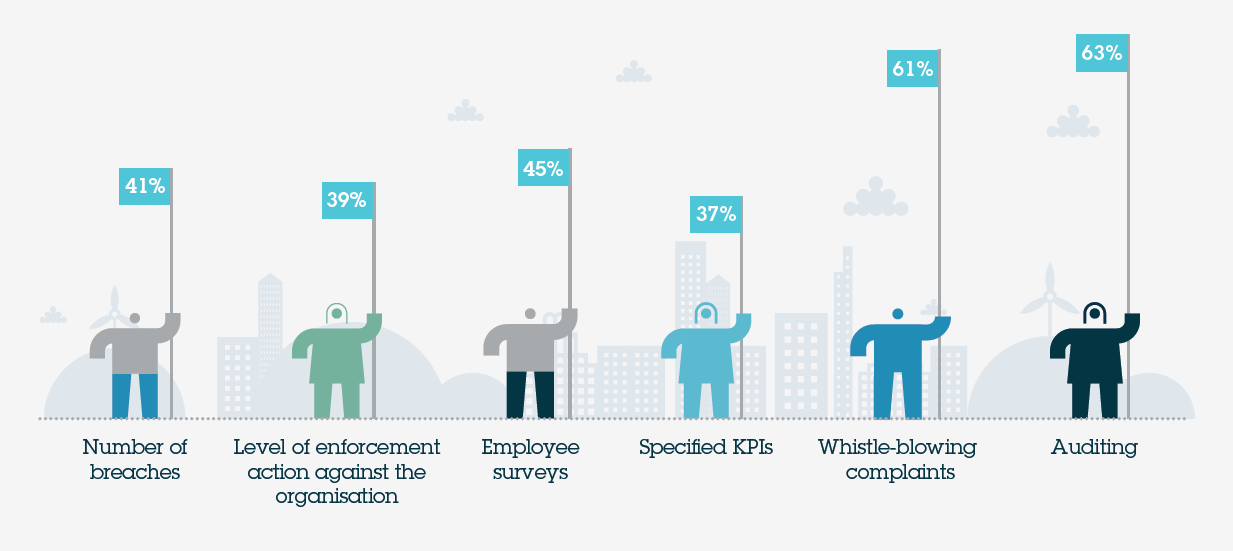

86% of respondents say that their organisation measures the effectiveness of its corporate legal compliance programme.

How does your organisation measure the effectiveness of its corporate legal compliance programmes? (Tick all that apply)

| "You can’t manage what you don’t measure," says Chris Wrigley, Co-Head of Global Compliance, Osborne Clarke. "Compliance needs better data in order to help the Board make timely decisions about the organisation. While it is good to see businesses using auditing as a measure of effectiveness, too often we see businesses fail to follow up on the results of an audit and make sure the recommended actions are carried out.""It is also concerning to see effectiveness measured by the lagging indicators of the number of breaches (41%) and the level of enforcement action faced by the company (39%). There is a risk that a business who has a low number of breaches or enforcement actions stops taking positive action to pro-actively look for ways to improve its compliance because it believes its existing systems are effective. These measures need to be balanced against employee surveys and specifiic KPIs that measure on-going compliance performance and are a way of driving continuous improvement." |

Almost 9 in 10 (86%) respondents say that their organisation measures the effectiveness of its corporate legal compliance programme. This increases to 98% of respondents both for those in legal/ compliance roles and in businesses with a turnover of £100 million plus.

For those who noted their organisation measures the effectiveness of its corporate legal compliance programmes, the most popular means of doing so:

- With auditing (63%)

- With whistle-blowing complaints (61%)

- With employee surveys (45%)

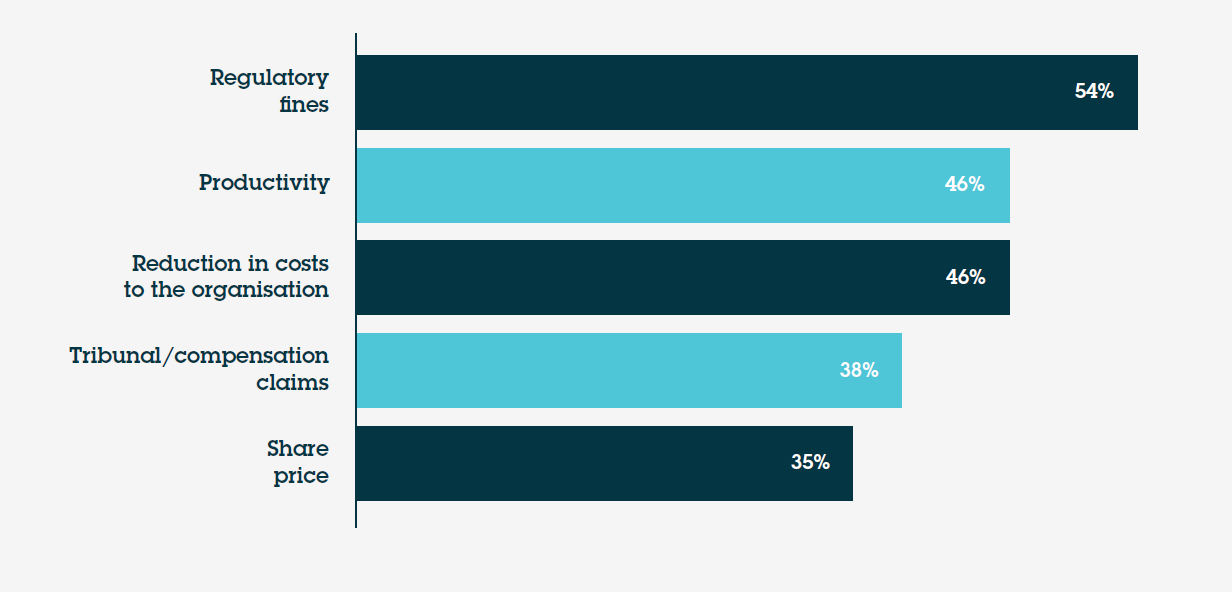

How does your organisation measure the financial return of its investment in corporate legal compliance? (Tick all that apply)

Regulatory fines – a key measure?

While 4 in 5 (80%) respondents said that their organisation measures the financial return of its investment in corporate legal compliance, there was a large discrepancy between Board/C-suite respondents and legal/compliance roles. 94% of those in legal/compliance roles said their organisation measures the financial return of its investment in corporate legal compliance compared to just over two thirds (67%) of those in Board/C-suite roles. While this may be further evidence of the communication gap between compliance roles and the Board, it perhaps also indicates that the Board/C-suite are less aware of the financial return that good compliance can bring.

Of the respondents whose organisation measures the financial return of investment in corporate legal compliance, over half (54%) are measuring this by the lagging indicator of regulatory fines. This is interesting when compared to measuring positive financial gains. For example, 46% measure by looking at reduction in costs to the organisations and the same percentage measure according to levels of productivity.

| Chris Wrigley sees positive and negatives in these figures. “It is encouraging that so many organisations are measuring the benefits of compliance. However, if that is not being communicated to the Board, it may be an opportunity missed. Regulatory fines are often a poor measure of the value of good compliance because they focus attention on the worst historic behaviour and only then if a regulator has identified the problem. While consistently poor compliance can cost an organisation a lot of time and money but still fall short of receiving regulatory fines. However, when fines are incurred, they can have a significant role in driving change throughout an organisation, particularly when they are significant and publicised. We’ve seen this in particular over the last few years. However, it is far more positive for an organisation to see that a robust compliance system is driving productivity and making the business more efficient by reducing costs.” |

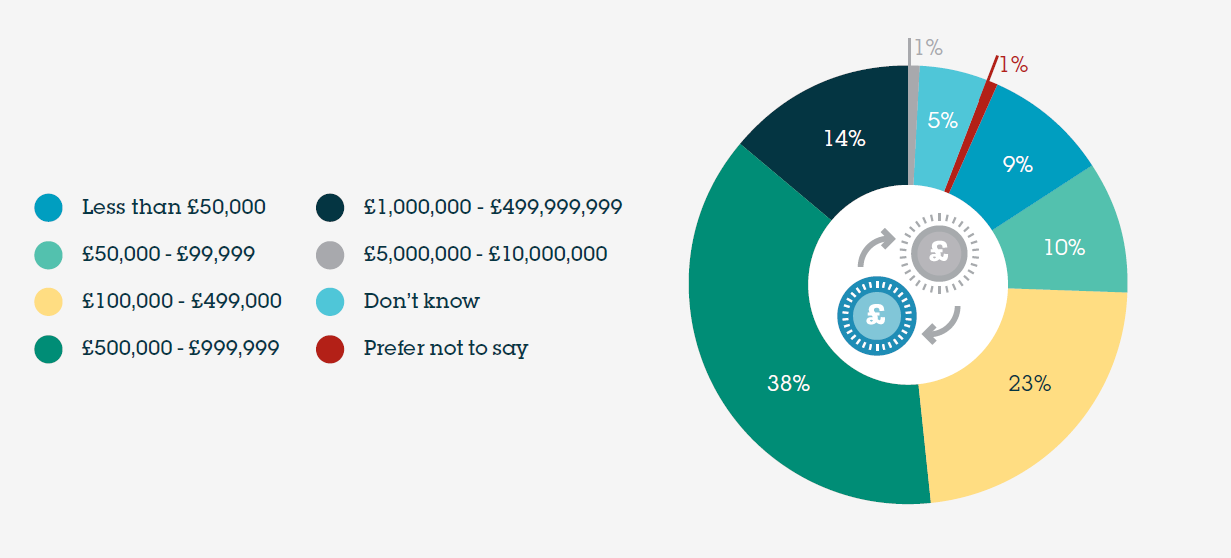

What would you estimate is the total financial return your organisation achieved through its corporate legal compliance programmes last year? (Tick one)

Significant returns

More than half (52%) estimate that the financial return their organisation achieved through its corporate legal compliance programme last year was £500k or above; and 15% estimate that it was between £1 million and £10 million. These significant returns indicate the value of effective and robust corporate legal compliance programme.

| "The financial value of good compliance can be very significant. It can be difficult to measure and is often challenging for our clients to explain to their stakeholders. But it is important for organisations to recognise the potential bottom line value of good compliance to the business,” says Chris Wrigley. |

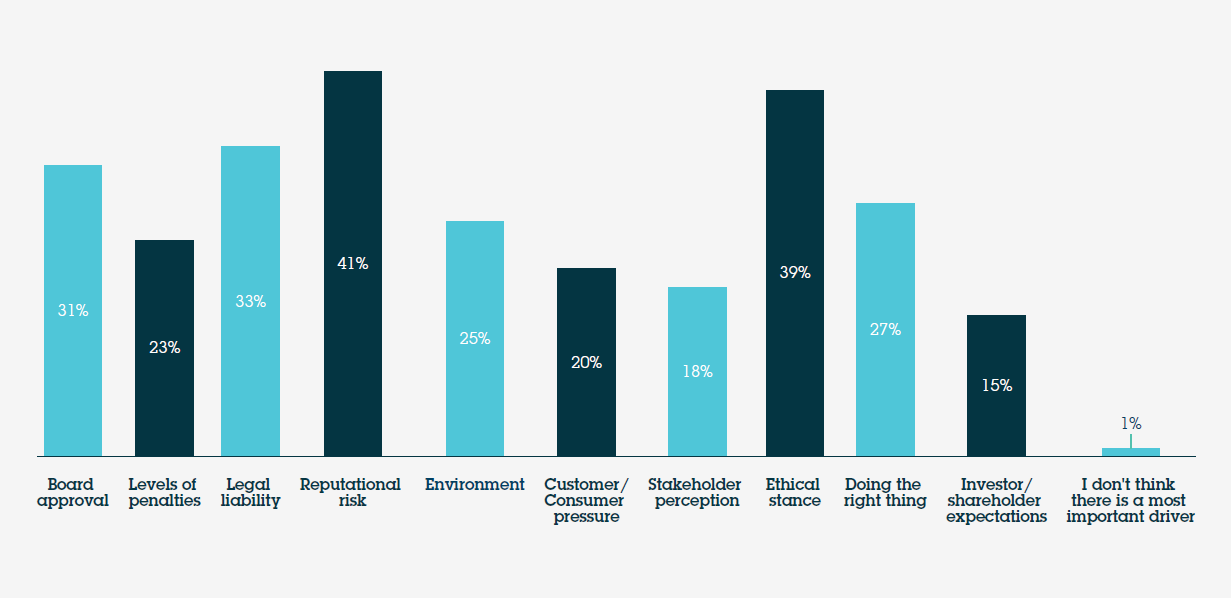

What do you think are the most important current drivers of investment in corporate legal compliance in your organisation? (Tick up to three)

Reputational risk and ethical stance key drivers of investment

2020 has shone a spotlight on business ethics and so it’s notable that almost 2 in 5 (39%) respondents said that one of the most important current drivers of investment in corporate legal compliance in their organisation was ethical stance. This is supported by the highest number of respondents (41%) identifying reputational risk as one of the most important current drivers of investment in corporate legal compliance. Yet despite reputational risk and an ethical stance being important, under 3 in 10 (27%) respondents said that one of the most important current drivers was doing the right thing. This could be viewed as indicating that businesses care more about perception than the action itself. It is also interesting that legal liability was selected by 33% of respondents and level of penalties was only selected by 23%.

| "Training on compliance areas often focuses on the legal implications and the level of potential fines. However, our survey suggests this is not what drives investment in corporate legal compliance. Senior business people know and understand the legal risk and consequences. But it is the corporate concern for reputation that is guiding compliance legislation around the world in a number of compliance areas. Governments have recognised the priority given by corporates to protection of reputation and are leveraging that corporate concern to drive change in areas such as modern slavery" concludes Chris Wrigley. |

Section 4: Barriers and impact on future investment

Over a fifth believe COVID-19 will have the single biggest impact on their organisation’s level of investment in corporate legal compliance in the next five years.

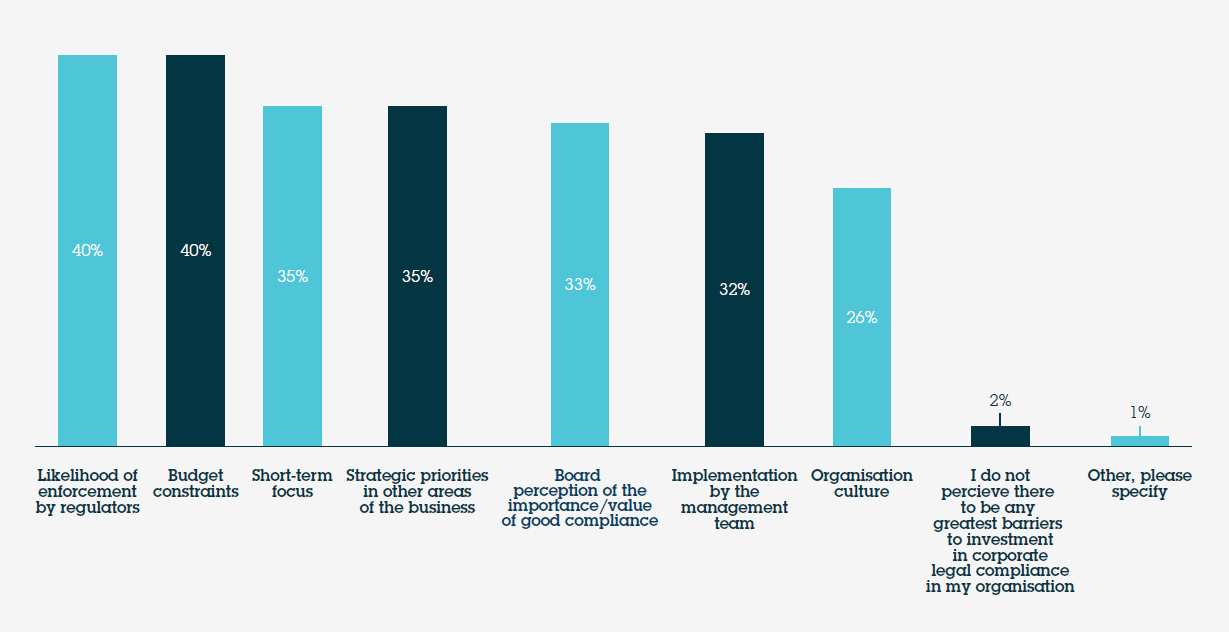

What do you perceive as the greatest barriers to investment in corporate legal compliance in your organisation? (Tick up to three)

Likelihood of enforcement by regulators is the greatest barrier to investment

2 in 5 (40%) respondents perceive one of the greatest barriers to investment in corporate legal compliance in their organisation to be the likelihood of enforcement by regulators.

| "This tends to suggest that if a business views the risk of enforcement as low, it is less likely to invest in that area of compliance," says Katie Vickery. "This is problematic for regulators who fpr the last few years have had enforcement budgets cut." |

Around a third of respondents see Board perception of the importance/value of good compliance (33%) and the way compliance is implemented by the management team (32%) as one of the greatest barriers to investment in corporate legal compliance. However, only 26% perceive organisation culture as one of the greatest barriers to investment in corporate legal compliance in their organisation. While this may indicate that just under three-quarters of respondents believe that they have the right organisational culture, just over a quarter are seemingly not receiving the right compliance message delivered from the top.

| "Having the right culture is such an important part of driving an effective compliance programme. But culture is led by the Board and by senior managers. If they don’t exemplify good practice around compliance issues then the rest of the business will follow their lead and pay lip-service to compliance issues," concludes Katie Vickery. |

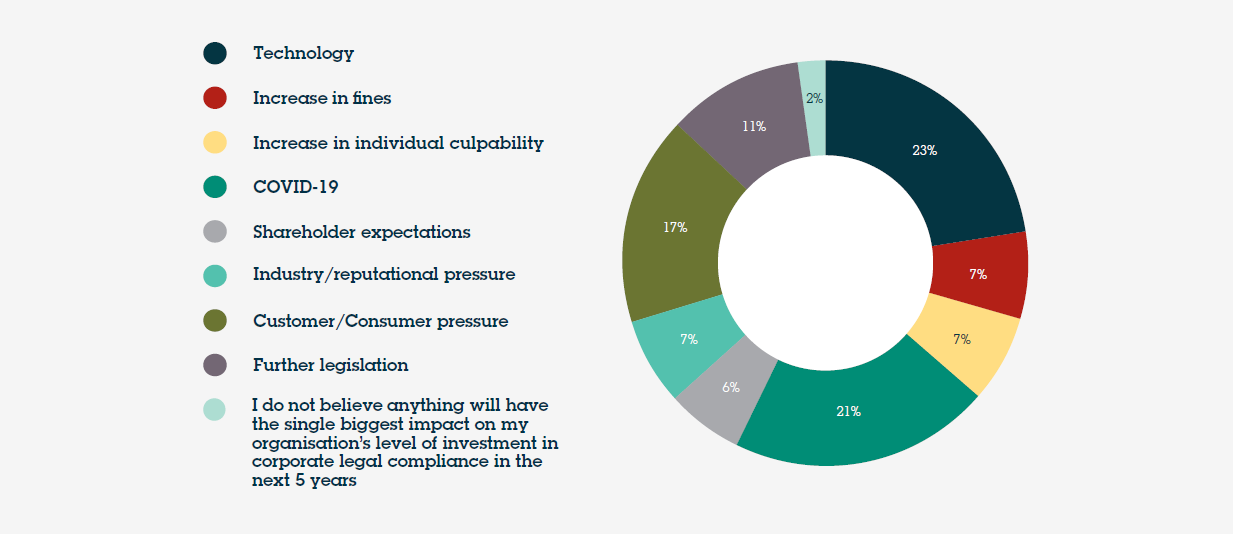

What, if anything, do you believe will have the single biggest impact on your organisation’s level of investment in corporate legal compliance in the next 5 years?

The theme throughout the data has been the impact that COVID-19 has had on business. This issue is also the second most cited influence that respondents believe will have the single biggest impact on their organisation’s level of investment in corporate legal compliance in the next five years (21%). Earlier data showed that respondents were driven by reputation and ethical stance and in this instance, over 1 in 6 (17%) believe that customer/consumer pressure will have the single biggest impact on their organisation’s level of investment in corporate legal compliance in the next five years. In comparison, and following the theme that the level of penalties is not a significant driver for investment in compliance, only 7% believe an increase in fines will have the single biggest impact on their organisation’s level of investment in corporate legal compliance in the next five years.

Technology will have the single biggest impact on investment levels

But it was technology that was the most cited influence respondents believe will have the single biggest impact on their organisation’s level of investment in corporate legal compliance in the next five years (23%). This echoes the data showing that technology had the highest average percentage for the amount of corporate legal compliance spend.

| "Technology is being used much more in compliance, either as a means to manage and keep track of compliance issues or as a tool to improve compliance processes,” says Katie Vickery. “The survey confirms what we are seeing in practice that innovative technology compliance tools are making it easier to apply systems and procedures. However, technology is only ever an enabler and is not a replacement for a robust compliance culture which is embraced by a senior management team.” |

Less than a quarter (24%) of respondents are confident that their company’s corporate legal compliance processes are as effective as they need to be but 25% think that COVID-19 will have a positive impact by forcing their company to be more legally compliant.

Meanwhile, almost 3 in 10 (29%) said their legal compliance programme is built around reacting to situations and only 16% agreed that their legal compliance programme pro-actively anticipated issues and put in place systems to deal with them.

| "We’d love to see that statistic around ‘compliance systems are as effective as they need to be’ climb rapidly from its current 24%. Our sense is that it’s possible with drive and the right investment and focus too,” says Katie Vickery. “Without doubt COVID-19 has had a huge impact on business and this will continue but hopefully in positive terms from a compliance perspective. Finally, it would be great to see businesses getting more on the front foot with compliance and looking for issues rather than applying the sticking plasters after an incident has happened. This aligns with the approach taken by regulators and prosecutors who increasingly expect to see pro-active, risk based compliance systems that actually work in practice rather than being a glossy set of policy documents that nobody follows.” |

Conclusion

This survey could not have come at a more interesting time. Businesses are adapting to a post-COVID-19 world while the end of the Brexit transition period approaches and a severe economic downturn sets in.

Do businesses have more important things to worry about than legal compliance? Even at the best of times “compliance” is a word guaranteed to receive eye-rolling and groans. The problem is compliance is often seen as a separate function (or, worse, the job of the “compliance team”) and as an adjunct to the actual running of a business to deliver a profit.

Businesses that have embraced compliance systems, as part of the foundations of the way they are run, have generally fared better in dealing with the changes going into and out of lockdown and planning for the next few years. As respondents to this survey have confirmed, compliance does have a financial value to businesses. It is important that this value is understood, so it can be leveraged to the benefit of businesses amid challenging economic conditions.

What does this survey tell us?

COVID-19 is expected to have a lasting impact on the way businesses approach compliance. The experience of the last few months will be part of planning and investment decisions not just for next year but for the next five years and probably permanently.

Technology is having a significant impact in the world of compliance – as it is in others – and businesses can expect to invest and use technology more as part of their compliance toolbox.

While data privacy continues to be a significant compliance risk for business, COVID-19 has drawn attention to the risks posed by other issues. Cybersecurity and health and safety are seen as increased risks. Businesses are also looking at their supply chain and the impact of environmental, social and governance factors.

Businesses are making investment decisions based more on how a compliance risk will affect their reputation and ethical stance than the threat of legal liability or the levels of fines. This may explain, in part, why consumer protection and product safety are seen as increased risks. They potentially can inflict significant damage to a business' reputation if something goes wrong. Regulators are certainly alive to this, and, at a time when they are working within

limited budgets, we should expect to see regulators taking more steps to “name and shame” non-compliant businesses rather than pursuing formal enforcement action.

There is a recognition by business that there is still much to do. Less than a quarter of respondents believe that their corporate legal compliance processes are as effective as they need to be; only 16% think that their compliance systems proactively deal with problems.

When businesses do get compliance right, the financial return can be significant and measured in the millions.

Do businesses have more important things to worry about? Every business will do its utmost to stay afloat during these challenging times ahead and will want to identify where money and resources are lost or wasted. Putting in place a better system or culture can help. There may be more important things to worry about, but good compliance systems can be part of the solution.

| Download > |

About the research

The research was conducted by Censuswide via an online survey in June 2020, with a sample of 101 respondents (aged 18-plus) with decision-making over their company’s corporate legal compliance processes in the UK only or across multiple jurisdictions. Fifty respondents are General Counsel/Head of legal, Chief Compliance Officers or In-house Lawyers and 51 respondents are Business Owners, CEO/Board Members, Chief Finance Officers, Chief Risk Officers or Other C-level Executives. 50% of the sample work at companies with a global turnover of less than £100 million and 50% of the sample work at companies with a global turnover of £100 million or more. We targeted the following sectors: Energy and Utilities, Life Sciences and Healthcare, Real Estate and Infrastructure, Retail and Consumer, Tech, Media and Communications, Transport and Automotive, Workforce Solutions.

Please note: In the text we regularly make comparisons between Board/C-suite roles and legal/compliance roles. Board/C-suite roles

include the job titles business owner, CEO/Board member, chief finance officer and other c-level executive. Legal/compliance roles include

general counsel/head of legal, chief compliance officer and in-house lawyer.

* Statistic combines ‘significantly increase’ and ‘slightly increase’

** Statistic combines ‘significantly decrease’ and ‘slightly decrease’

*** Statistic combines ‘strongly agree’ and ‘somewhat agree’

**** Statistic combines ‘increased by up to 25%’, ‘increased by 26% to 50%’ and ‘increased by more than 50%’

***** Statistic combines ‘decreased by up to 25%’, ‘decreased by 26% to 50%’ and ‘decreased by more than 50%’

Censuswide

Censuswide specialises in robust, high quality market research; offering both quantitative and qualitative research methodologies. Censuswide delivers accurate results in line with our clients’ brand message and is trusted by media as a credible source of market research data. We are proud to have an impressive reach with a depth of network from C-suite to full-time parents across 65 countries. Censuswide is a member of ESOMAR – a global association and voice of the data, research and insights industry. We comply with the Market Research Society code of conduct based on the ESOMAR principles.

About Osborne Clarke

Osborne Clarke is a future-focused international legal practice with over 750 talented lawyers and 250 expert Partners across 25 locations. We help clients across eight core industry sectors to succeed in tomorrow’s world. Our well-connected international group means we can offer the very best of Osborne Clarke’s sector-led approach and innovative culture wherever in the world you interact with us. And we have a robust understanding of the local business environment and in-depth legal expertise in each jurisdiction. We’re listeners, innovators and problem solvers, finding new ways to join the dots between our clients’ challenges today and the opportunities being created in an ever-evolving, ever- developing global society.

Our Global Compliance service

Prioritising and managing compliance risks across your business requires efficient, practical systems and a strong compliance culture. There is no 'one size fits all' solution. Some risks will will be more pressing, some will be better understood by the business than others, and many will overlap.

We can help you improve compliance and reduce your risks. We work with you to develop a holistic approach to your compliance systems, based on our deep understanding of regulatory regimes and our experience of assessing regulatory risk.

As an international legal practice, we see first-hand how compliance systems actually play out in practice. We have lived through the investigations and court hearings. We know what works and what does not, and can help contain the damage when things have gone wrong.

A dynamic system with a pro-active culture is at the core of good compliance. Compliance is never achieved through systems alone. It requires a willingness by everyone in the business to comply. We work with you to develop a collaborative approach and a committed leadership.

In a global economy you need a global approach to compliance. Our international team will make sure that your system works locally and across all of the markets in which you operate.

Our four-step approach:

| Download > |

{kind=link}