PSR publishes decision paper and further consultation on regulatory fees for 2018/19

Published on 13th July 2021

On 28 March 2018, the PSR and FCA published a combined consultation and decision paper on PSR regulatory fees for 2018/19 (CP18/8). The decisions, which will take effect from 2018/19, change the way in which PSR fees will be calculated. They also implement further changes to enable the FCA to calculate, bill and collect fees from PSR fee payers (including PSPs) directly, rather than relying on payment system operators to collect PSR fees on the FCA's behalf.

The consultation and decision paper sets out the decisions on the questions the PSR asked in CP17/44 relating to:

Further consultation issues about fees and refund

As well as changing the formula for fee allocation, the PSR makes further proposals on its fees allocation method relating to: (i) its approach to publishing annual fees figures in future; (ii) updated definition of relevant transactions for fees allocation; (iii) its approach to on-account fees collection from 2019/20 onwards; and (iv) refund of underspend, including the 2017/18 underspend.

The FCA expect to issue a policy statement in summer 2018.

Amendments to FEES 9 rules in the FCA Handbook

Separately, the FCA has published the Fees (Payment Systems Regulator) Instrument (No 6) 2018 (FCA 2018/9), made by the FCA Board on 22 March. The instrument came into force on 1 April 2018 and makes amendments to FEES 9 and the Glossary in the FCA Handbook.

The FCA will calculate, bill and collect PSR fees from PSR fee payers directly, and the operators of payment systems will no longer be required to bill and collect fees from PSR fee payers.

Further consultation issues about fees and refund

As well as changing the formula for fee allocation, the PSR makes further proposals on its fees allocation method relating to: (i) its approach to publishing annual fees figures in future; (ii) updated definition of relevant transactions for fees allocation; (iii) its approach to on-account fees collection from 2019/20 onwards; and (iv) refund of underspend, including the 2017/18 underspend.

The FCA expect to issue a policy statement in summer 2018.

Amendments to FEES 9 rules in the FCA Handbook

Separately, the FCA has published the Fees (Payment Systems Regulator) Instrument (No 6) 2018 (FCA 2018/9), made by the FCA Board on 22 March. The instrument came into force on 1 April 2018 and makes amendments to FEES 9 and the Glossary in the FCA Handbook.

The FCA will calculate, bill and collect PSR fees from PSR fee payers directly, and the operators of payment systems will no longer be required to bill and collect fees from PSR fee payers.

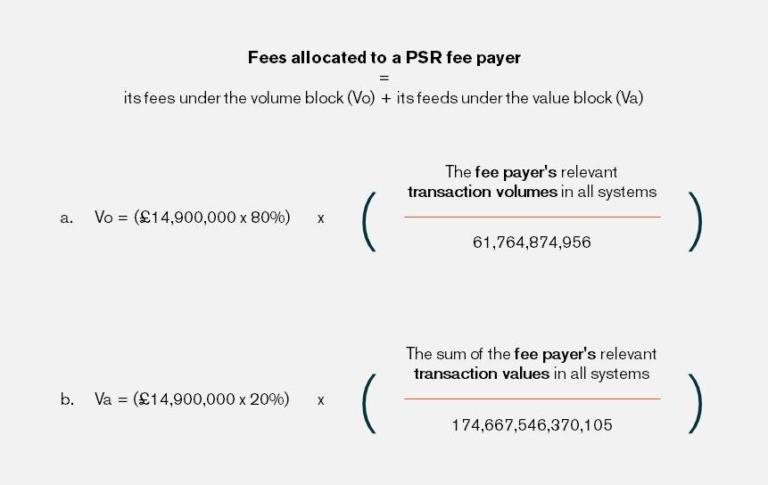

- the fees allocation method, including the proposal to allocate PSR fees based on fee payers’ transaction volumes and values; and

- the fees collection method, in particular the provision of transaction data by operators, the verification of transaction data and the provision of contact details and the payment dates.

Further consultation issues about fees and refund

As well as changing the formula for fee allocation, the PSR makes further proposals on its fees allocation method relating to: (i) its approach to publishing annual fees figures in future; (ii) updated definition of relevant transactions for fees allocation; (iii) its approach to on-account fees collection from 2019/20 onwards; and (iv) refund of underspend, including the 2017/18 underspend.

The FCA expect to issue a policy statement in summer 2018.

Amendments to FEES 9 rules in the FCA Handbook

Separately, the FCA has published the Fees (Payment Systems Regulator) Instrument (No 6) 2018 (FCA 2018/9), made by the FCA Board on 22 March. The instrument came into force on 1 April 2018 and makes amendments to FEES 9 and the Glossary in the FCA Handbook.

The FCA will calculate, bill and collect PSR fees from PSR fee payers directly, and the operators of payment systems will no longer be required to bill and collect fees from PSR fee payers.